Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BASIC INDUSTRIES

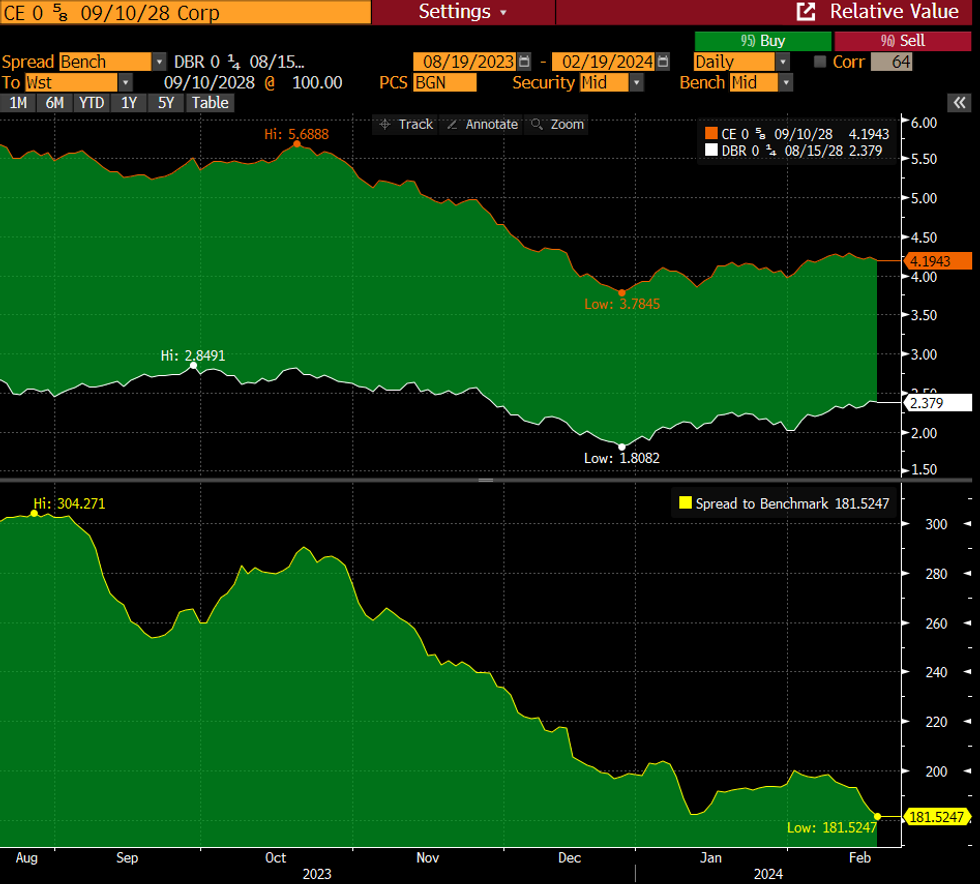

- Consensus expects FY2023 revenue growth of ~ +14% YoY with EBITDA ~+8%. With meaningful exposure to Autos and particularly EVs the outlook will be closely watched. At 3Q the company was guiding for stabilising demand in challenging conditions.

- Back at 2Q Celanese missed expectations, triggering a change to outlook negative at S&P (BBB-). This has left CE on the fallen angel watchlist since.

- Markets found relief in Celanese’s better 3Q results which focused on deleveraging, with spreads rallying ever since. CE 5.337 29 currently sit at new tights.

- While there is still some premium in CE relative to rating comps we would expect that to persist for a cyclical reverse Yankee issuer. We can infer that market expectations are pricing a downgrade as low probability currently.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok