Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

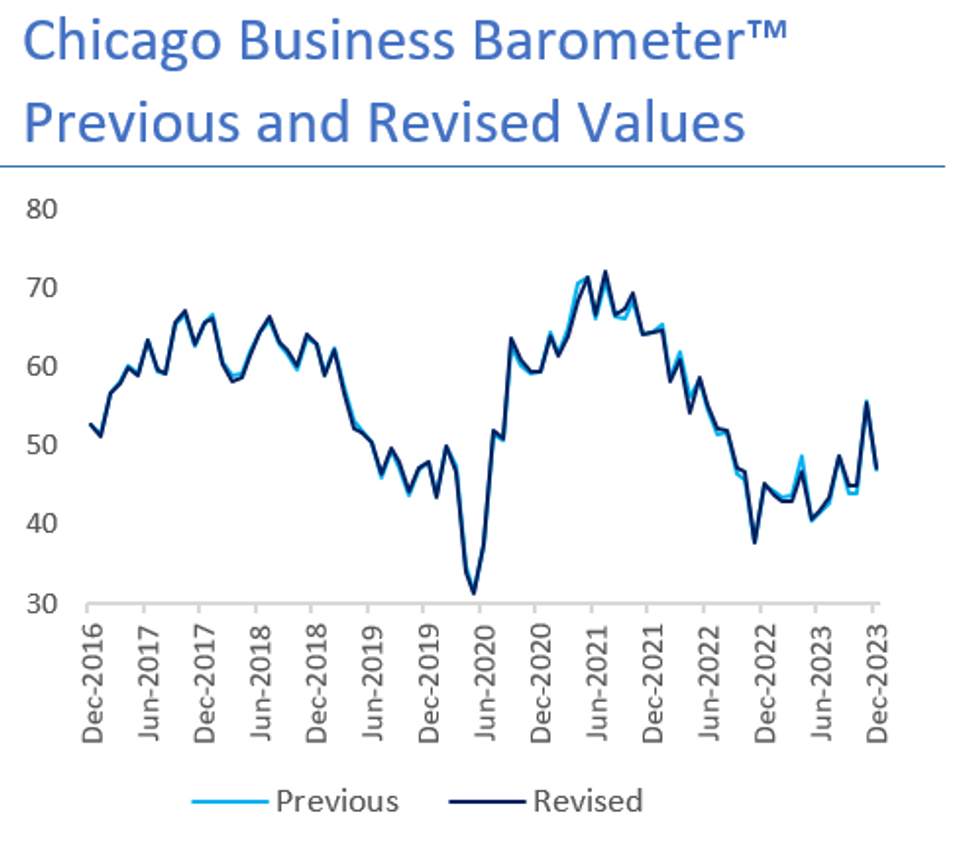

Chicago Business BarometerTM, produced with MNI, was revised up to 47.2 in December from 46.9, as result of the annual seasonal adjustment recalculation. Growth in the first half of the year was slightly softer than previously estimated while the second half of the year – Q3 in particular – was stronger than previously estimated.

- April saw the largest downward revision, with the Barometer revised lower -1.8 points to 46.8 from its initial estimate of 48.6, while October recorded the biggest upward revision of +1.0 point to 45.0.

- Although the Barometer remained below 50 most of the year, Q3 showed a softer pace of contraction that extended to Q4, with the Barometer revised up to 45.8 in Q3 (+0.6 points) and to 49.3 in Q4 (+0.4 points).

- Order backlogs saw the largest upwards revision (+2.5 points) followed by Employment that was revised higher by +1.1 points in December to 46.2.

- New Orders were little changed, while Production also saw a small revision to 58.6 (-0.2 points).

- Supplier Deliveries was revised lower by -0.8 points.

- Prices remained high but expanded at a lower rate by the end of the year, with the Prices Paid Indicator revised lower by -2.0 points to 68.0.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok