Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

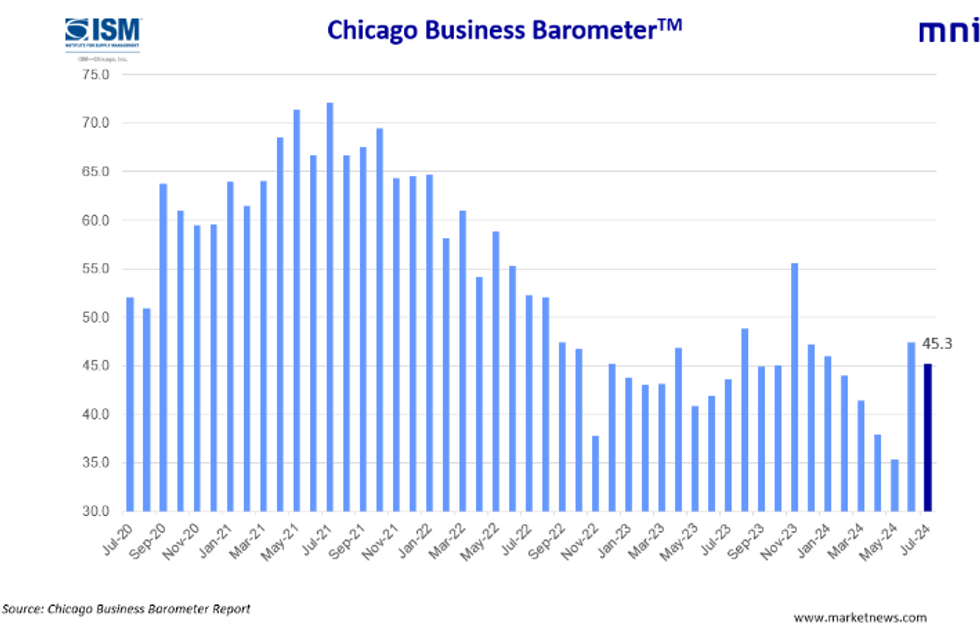

The Chicago Business Barometer™, produced with MNI slipped 2.1 points to 45.3 in July, after rising in June for the first time since November 2023.

- The fall was broad based with four out of five subcomponents down, in comparison to all five components rising last month. Production led the deterioration this month, with New Orders, Order Backlogs and Employment also lower. Meanwhile, Supplier Deliveries edged up.

- Production fell 8.2 points to 46.4, making it the lowest since May 2024. Respondents have become increasingly polarized.

- New Orders declined 2.5 points, after jumping up 16.9 points in June.

- Order Backlogs lessened by 2.8 points, also after it recorded a large rise of 14.2 points in June.

- Employment slowed by 2.2 points to 41.9. This was due to the proportion of respondents reporting lower levels of employment increasing.

- Meanwhile, Prices Paid curtailed a further 0.7 points to 55.8, taking it to the lowest level since June 2023.

- Supplier Deliveries rose for the third consecutive month by 5.1 points to the highest since November 2023.

- Finally, Inventories fell 4.0 points, after reaching the highest levels seen since November 2023 last month.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok