Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (London)

Key Points – September 2022 Report

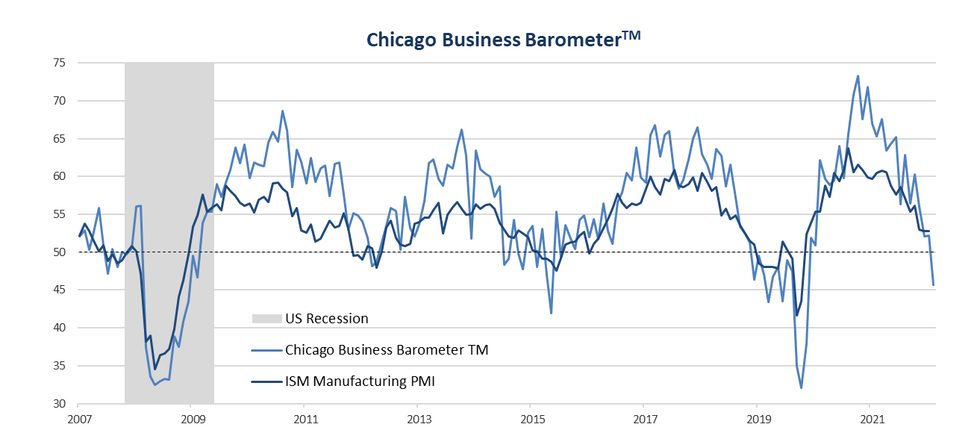

The Chicago Business Barometer™, produced with MNI, declined to a more than two-year low in September. The indicator tumbled by 6.5 points to 45.7, entering contraction territory for the first time since June 2020.

- All main indicators fell in September, with production, neworders, order backlogs, employment and supplier deliveriesall weakening to Summer 2020 lows. The largest declineswere recorded in employment, order backlogs andproduction sub-indices.

- Production slumped by 10.4 points to 44.5 in September,giving back all the recovery (and more) from August.Continued supply-chain issues alongside slowing new orderscontributed to lower production for the month, experiencedby over a quarter of respondents.

- New Orders contracted for the fourth consecutive month,slipping by 6.7 points to 42.2. Softening demand was cited.• Order Backlogs slowed 12.6 points to 41.9 as weak neworders saw production shift to working through remainingorders.

- Employment recorded the starkest decline in September,dropping 14.4 points to 40.2 in September and re-enteringcontractive territory.

- Supplier Deliveries moderated by a further 2.3 points to59.8. This was the lowest since July 2020 as deliveriesremained unstable and lead times long.

- Inventories weakened by 8.6 points to 53.0, over five pointsbelow the 12-month average. Inventories remain very high,as firms cite having overstocked previously due to suppliesissues. As demand for materials slows alongside lower salesprojections, suppliers are requesting orders to maintainrelationship.

- Prices Paid softened in September by 7.7 points to 74.1.Price Paid was the lowest since November 2020 and signals amore substantial slowing of prices charged related to an earlysign of contracting demand in specific products.

SPECIAL QUESTION

This month we asked firms whether they were consideringnew hires into the second half of the year. Around 41% were,however half of these were looking to hire less than originallyplanned. A total 33.3% were holding off on new hires. Aminority of 2.6% anticipated severances, while 23.1%remained unsure of employment plans for H2.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok