Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

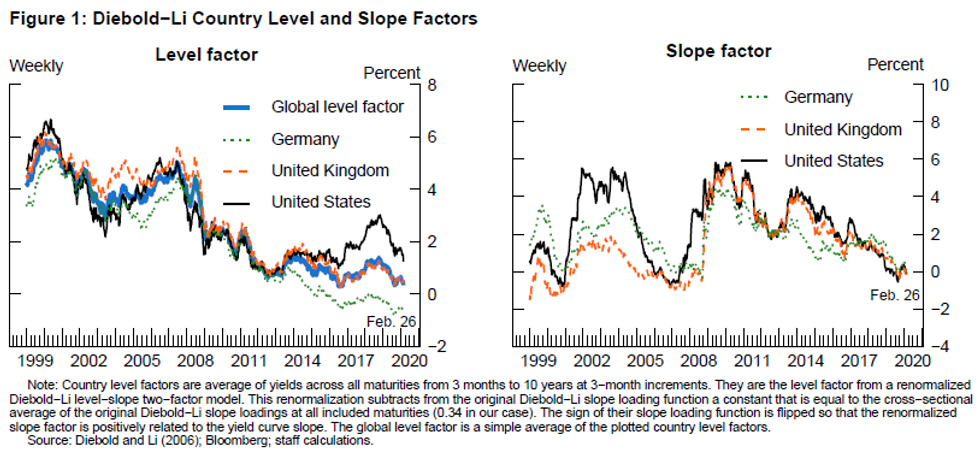

Nothing on current monetary policy in Fed Vice Chair Clarida's speech today, with his focus instead on the academic literature on global yield curves - and what monetary policy can and cannot control. It can control the "slope" of the yield curve, but not so much the "level".

- "credible inflation-targeting central banks operating in an integrated global capital market—at least when they are operating away from their effective lower bound (ELB)—are primarily in the yield curve "slope" business, but much less so in the yield curve "level" business"

- "over the past 20 years, more than three-fourths of the variance of the Treasury slope factor can be accounted for by the policy rate spread [the spread between the US neutral nominal policy rate and the actual Fed funds rate], which is obviously something the Federal Reserve can control when it sets the federal funds rate."

- The "level" - changes of which are known to bond traders as "parallel shifts" in the yield curve - is "plausibly" reflective of several global macro drivers, "including global productivity growth, the balance between global saving and investment, and longer-term inflation expectations"

- So, central banks can't do much to control the level of yields, but can control the shape of the curve - and that, Clarida says, is important for central banks who want to distinguish the "signal from noise from sovereign yield curves as well as for how they calibrate the stance of monetary policy consistent with a credible inflation target."

Source: Federal Reserve

Source: Federal Reserve

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok