Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

The South Korea April consumer confidence headline was unchanged at 100.7. We are comfortably above mid 2022 lows near 86, although the trend improvement in the headline index has stalled in recent months, which suggests a steady rather than accelerating GDP growth backdrop.

- In terms of the detail, we didn't see a lot of change to the sub-indices. Some slight improvement in terms of the domestic economy (81 from 80 prior) was offset by slightly lower spending intention plans (110 versus 111 in March).

- On the prices front, we saw house price expectations jump to 101 from 95 prior, while expected wages also rose a touch to 117, from 116. This measure remains within recent ranges though.

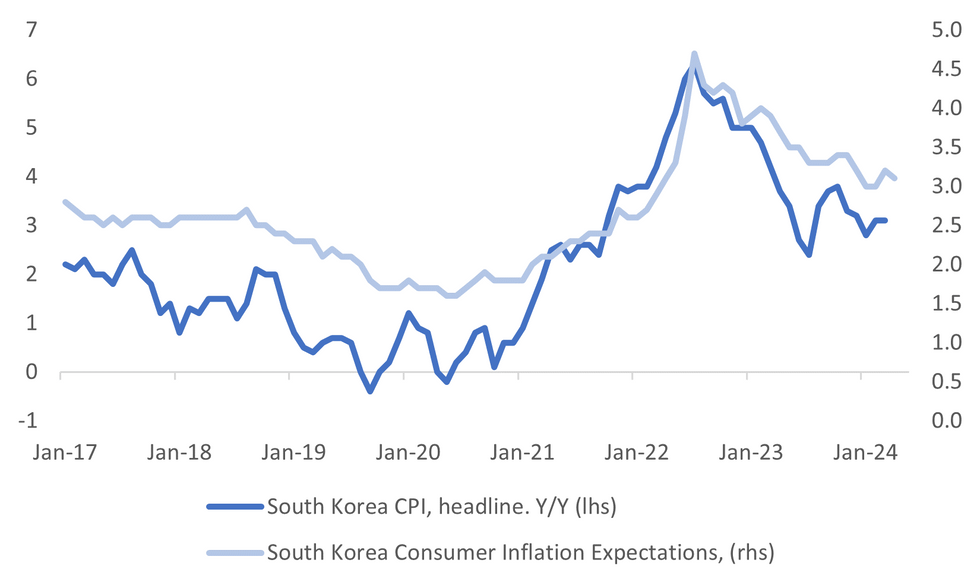

- Expected inflation eased modestly to 3.1% from 3.2% prior. The chart below overlays this expectations measure against headline CPI y/y.

- This is a modest improvement, but the trend towards 2% (BoK's inflation target) has stalled to a degree. The BoK is likely to want to be more confident of such trends before easing policy, which is its H2 bias. note the next CPI print, for April, is out on May 2.

Fig 1: South Korea Inflation Expectations Versus CPI Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok