Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

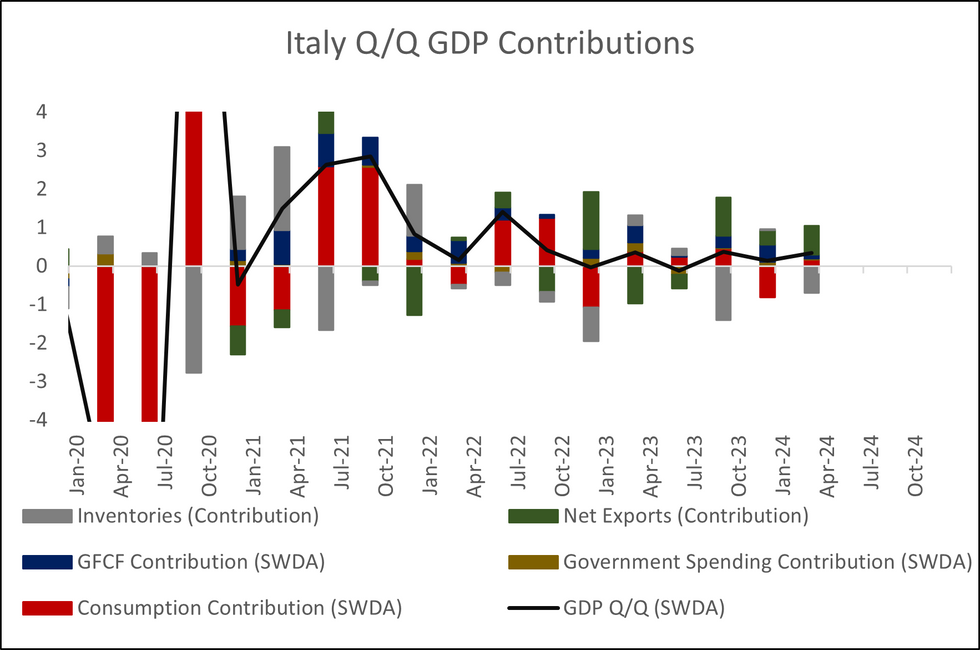

Italy quarterly Q1 GDP confirmed flash estimates at 0.3% Q/Q (vs 0.1% prior), while the annual figure was revised a tenth higher to 0.7% Y/Y (vs 0.7% prior).

- The details of the final release confirm that net exports were the largest contributor to GDP in Q1, adding 0.7pp to the quarterly growth rate.

- However, we note that inventories dragged down the domestic demand component by 0.7pp, offsetting the positive effect from net exports.

- That means that domestic demand ex-inventories contributed 0.3pp in total: Consumption 0.2pp, investment 0.1pp and government spending 0.0pp.

- The positive contribution of consumption comes despite weak developments in retail sales and consumer confidence through 2024. The resilient labour market, where the unemployment rate recently reached a new all-time low, likely supported consumption in Q1.

- Indeed, consumption printed above consensus expectations on an annual basis at 0.1% Y/Y (vs -0.2% cons). At present, analysts expect a -0.2% Y/Y development in Q2, but these estimates may be revised higher in time.

- Additionally, the 0.5% Q/Q growth in gross fixed capital investment was driven by a 1.7% Q/Q rise in construction investment (probably a function of the well-documented and controversial Superbonus scheme).

- We will return with an analysis of the GDP deflator and its components early next week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok