Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

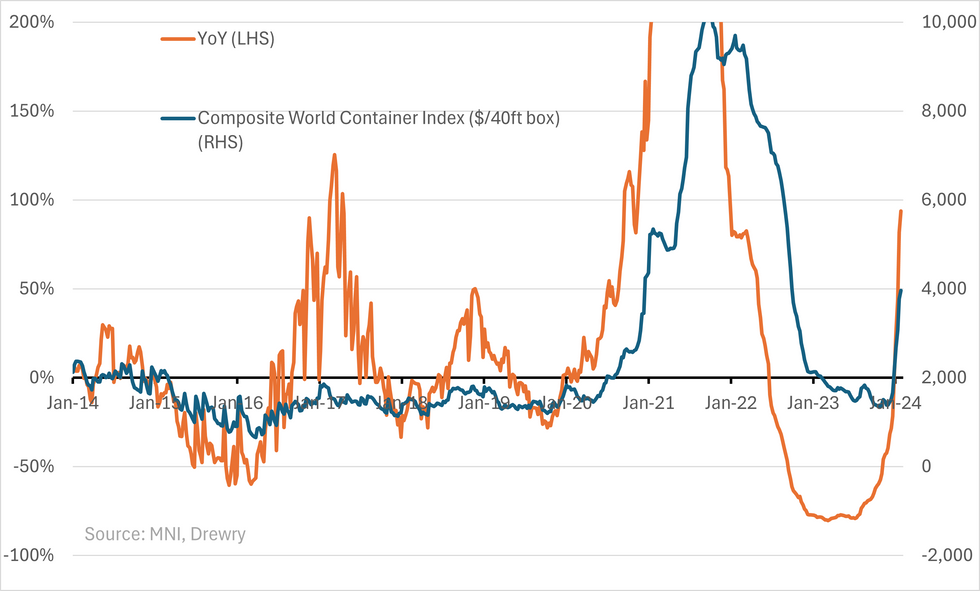

Container rates came in relatively flat WoW - ECB's Lagarde dismissing it in Q&A but headlined a bit more in the UK PMI report that flagged impact of fright on rising manufacturing costs. Impact on Oil was limited - that's reversed a little this week with WTI up 5%- our commods team see it linked to Red Sea escalation but also in part due to attacks on Russian energy infra & China stimulus - some of this passed through to breakevens which have continued trending higher this year - some of this might be technical factors on the back of aggressive rates sell-off.

On the flipside today's Q4 Core PCE was supportive of inflation staying within Fed target - but it doesn't capture any of the increase in shipping which came this year. Drewry's remarks were supportive of more easing to come "expect spot rates to plateau or decline in the next few weeks on the routes from Asia." - the rates from Asia (to Europe) are the main ones effected by the Red Sea disruptions. We will continue seeing YoY increases if container rates hold flat from base effects last year (rates were falling -2%/week this time last yr).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.