Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KRW

1 month USD/KRW sits close to session highs currently, last near 1305 (highs were close to 1306.30), which is +0.30% on NY closing levels. This comes despite a weaker USD tone against the majors, albeit a modest one, while regional equities are higher (Kospi +0.96%).

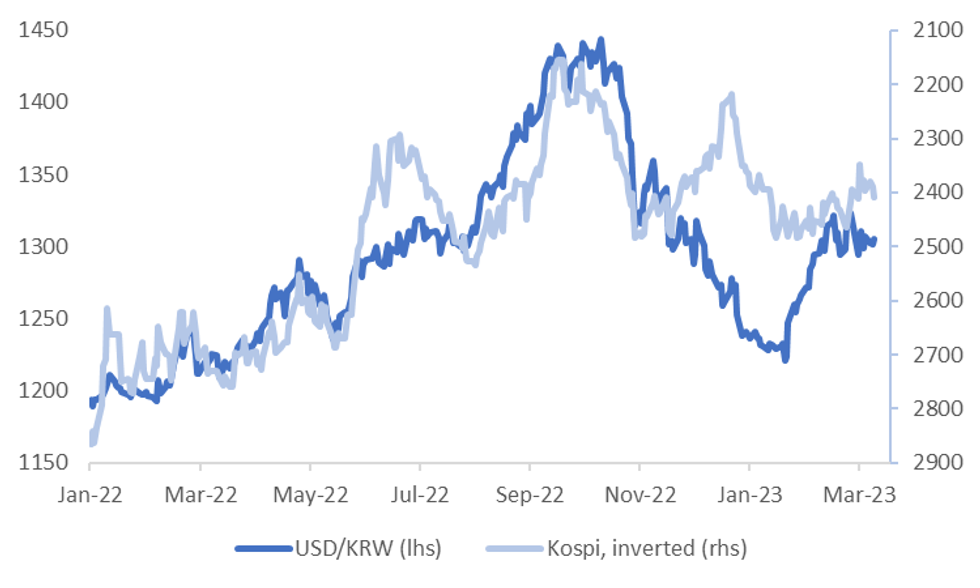

- The relationship between KRW and the Kospi has not been as strong in recent months, see the first chart. The current rolling 1 month correlation (in levels) is close to flat. For much of 2022 we were consistently in the -60/-80% range (i.e. higher local equities coincided with lower USD/KRW levels).

- One possible driver of this weaker correlation has been the shift in the National Pension Service (NPS) FX hedging policy. The authority was asked to raise the ratio to 10% late last year to help curb USD demand.

- Also note corporate FX deposits fell sharply in Feb, down nearly $12bn, the sharpest drop since 2012, which also be impact local FX supply/demand dynamics.

- So, it remains to be seen when this correlation (between equities and the KRW) re-asserts itself.

Fig 1: USD/KRW Versus Kospi (Inverted)

Source: MNI - Market News/Bloomberg

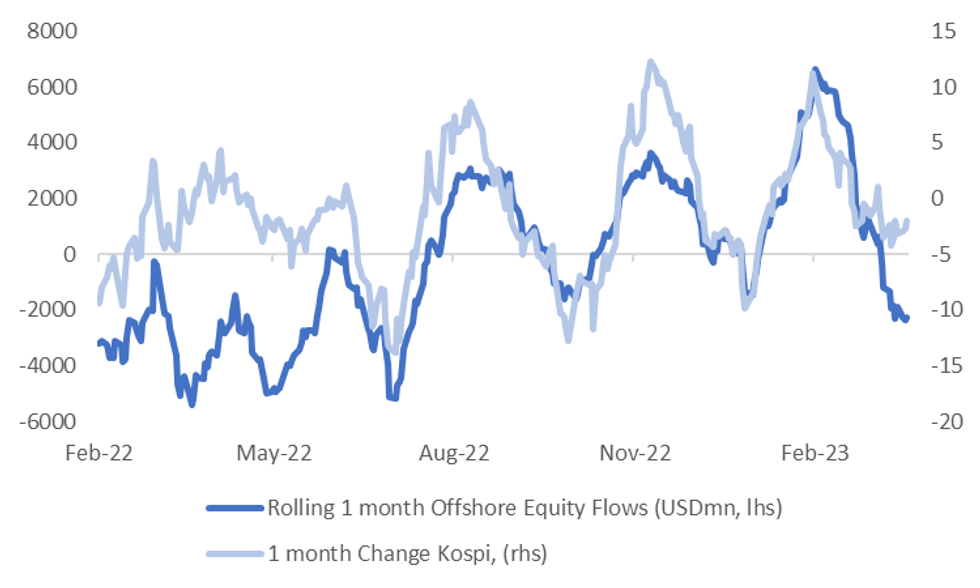

- It's also noteworthy that offshore equity flows have yet to return in a meaningful way, despite the Kospi being on a more stable footing in recent trading, see the second chart below.

- All else equal, this will provide less flow support for the won, than otherwise might be the case. An improved flow picture can aid the won and perhaps help drive a fresh test sub 1300, but the market will likely want to see how the Fed decision unfolds later before flows return in a meaningful fashion.

Fig 2: Kospi (1 month change) Versus Offshore Equity Flows (Rolling 1 month sum)

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok