Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

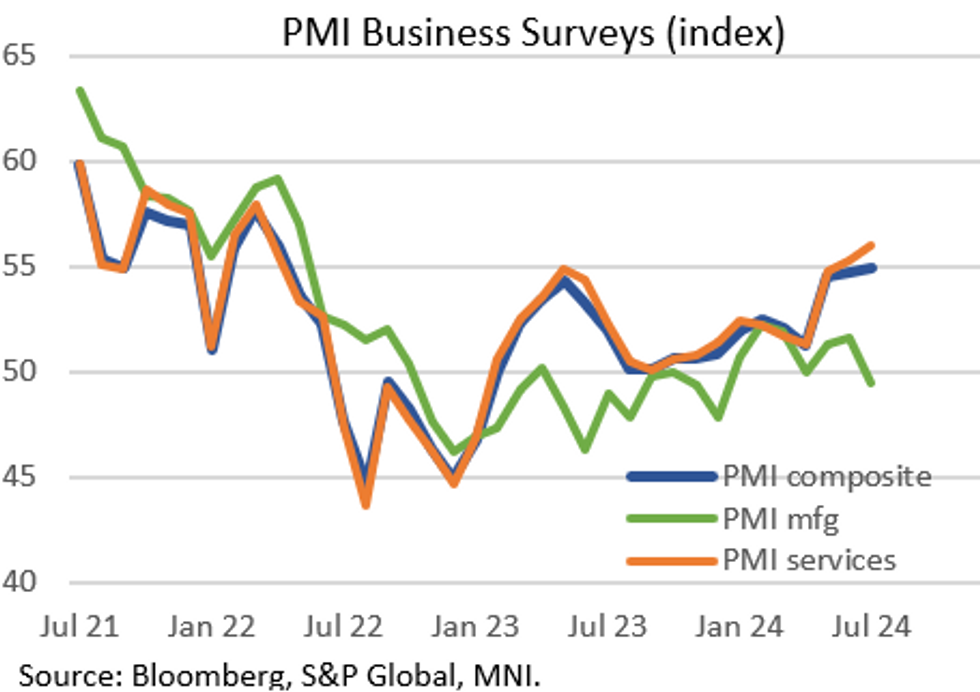

US PMI readings continued to diverge in July's flash report: the Manufacturing reading unexpectedly fell into contractionary territory at 49.5 (51.6 expected and prior), with Services unexpectedly rising to 56.0 (54.9 expected, 55.3 prior).

- The Services reading was the highest since March 2022, maintaining the upward momentum seen in the sector since 3Q 2023, while Manufacturing was the weakest (and first contractionary) reading since December 2023.

- The S&P Global report noted that the data is consistent with GDP growth of 2.5% annualized (vs 2.0% signaled by PMIs for 2Q - we get national accounts data Thursday), while the prices charged gauges are consistent with the Fed's 2% target.

- S&P Global also notes that this was the biggest gap between the two readings since June 2023, though some of the manufacturing weakness "was linked to staff shortages, so could prove temporary". Some highlights from the report, which further underline this divergence:

- Inflation: "Competitive forces ... meant prices charged for goods and services rose at one of the slowest rates seen over the past four years [slowest rate since January, and the second-slowest rate since October 2020], though some renewed upward pressure on costs was reported. Input prices across goods and services rose at the steepest rate for four months."

- Employment/Confidence: "The positive news was further marred by employment growing at a slower rate, and business confidence in the outlook falling for a second month, fueled in part by rising political uncertainty ahead of the Presidential Election."

- New Orders: "Measured overall, inflows of new work rose at a slightly reduced rate, caused by a renewed fall in new orders at manufacturers. However, the overall rise was the second largest seen over the past 13 months thanks to faster inflows of new business placed at service providers, which rose at the sharpest rate for just over a year."

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok