Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China October inflation data prints today. Headline CPI is expected to ease to 2.4% from 2.8% (the range of forecasts is 2.0-3.0%). For PPI, the consensus is -1.5% (with a range of +1.0 to -1.7%).

- Outside of food inflation, CPI pressures have been fairly modest. With pressure on the food front expected to moderate this should help ease overall CPI pressures. Recall last month that core inflation eased to 0.60% y/y, fresh lows back to early 2021.

- On the PPI side, upstream price pressures are expected to be weighed on by base effects. Last October the y/y print was +13.5%. Still, weakness in the property sector, coupled with softer onshore commodity prices (like steel etc) is also expected to present a headwind.

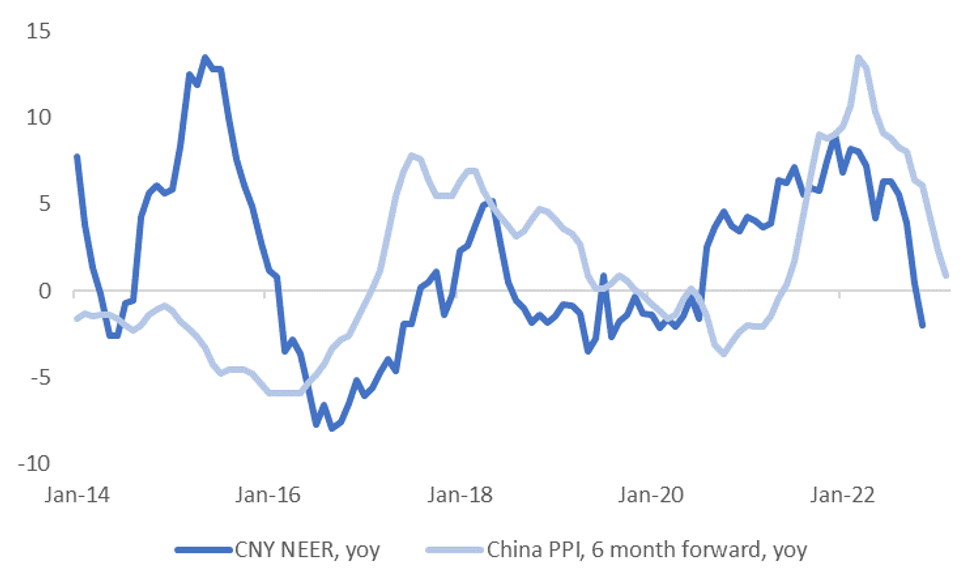

- Weaker inflation pressures, all else equal, argues for looser financial conditions overall in China. The chart below plots the PPI y/y, 6 months forward. against the CNY NEER (J.P. Morgan Index).

- The CNY NEER is already in negative y/y territory based off further weakness in November (down another -0.81% from end October levels).

Fig 1: China PPI Y/Y Versus CNY NEER Y/Y

Source: J.P. Morgan/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok