Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

Today's CPI reading pretty much eliminates any lingering chance the Fed could signal in November that it would slow the pace of hikes at an upcoming meeting. A 75bp hike on Nov 2 is a lock (77bp priced), and the baseline expectation will now be 75bp at the December FOMC meeting too (64bp priced), getting rates to 4.50-4.75%. That only gets us slightly beyond market pricing (140bp total by end-Dec).

- We get two more CPI readings between now and the Dec. 14 decision - one of those releases (for Nov CPI) is Dec 13th, and it would take a big surprise to sway the Committee from whatever it signals pre-blackout.

- 50bp is currently looking a little more likely than 25bp for February, which would get rates to 5.00-5.25%. That could end up being the terminal rate, but expecting a slowdown in hike pace to 25bp by the Feb 1 decision (30bp now priced in to a 4.8% rate, or 170bp from here) is a bet on CPI pulling back sharply by the end of the year (the Dec CPI report is out Jan 12th).

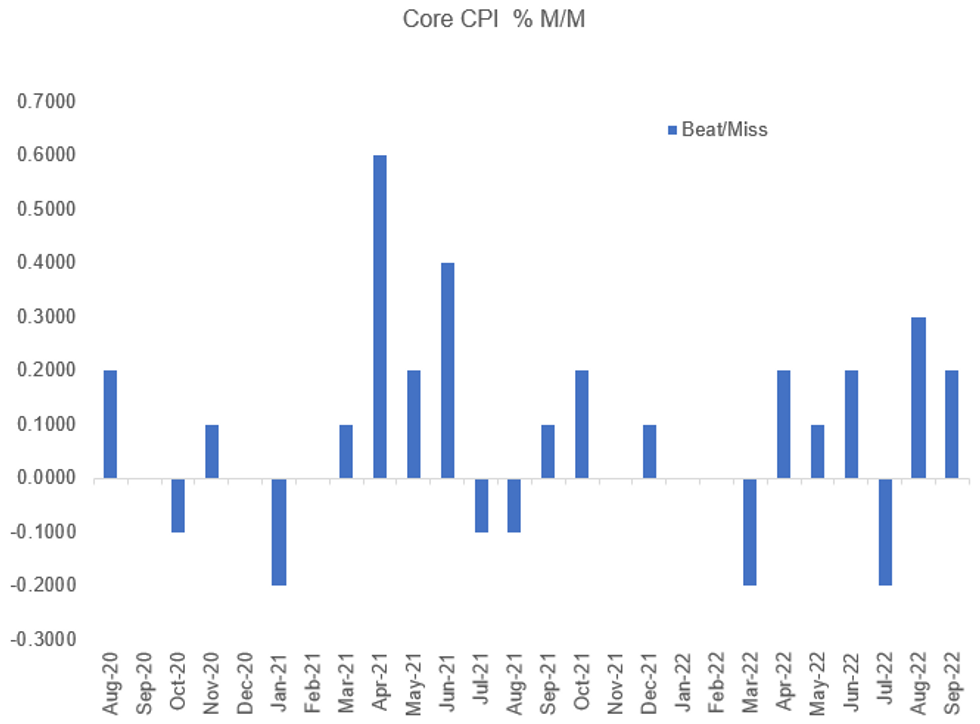

- Overall that's a tough bet: core CPI has beat expectations 5 of the past 6 months (see chart), and while core goods prices are soft, services are high and sticky.

- We'd thought previously that the December FOMC was the earliest we could see a "pivot" toward slowing the hike pace, but today's data makes it more likely to take into at least the mid-January CPI. The Fed reiterated its data dependence in yesterday's minutes and can't signal it will let up until getting clearer evidence of inflation slowing. Or, of course, we get a major crisis that collapses inflation expectations.

Source: BLS, BBG, MNI

Source: BLS, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok