Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

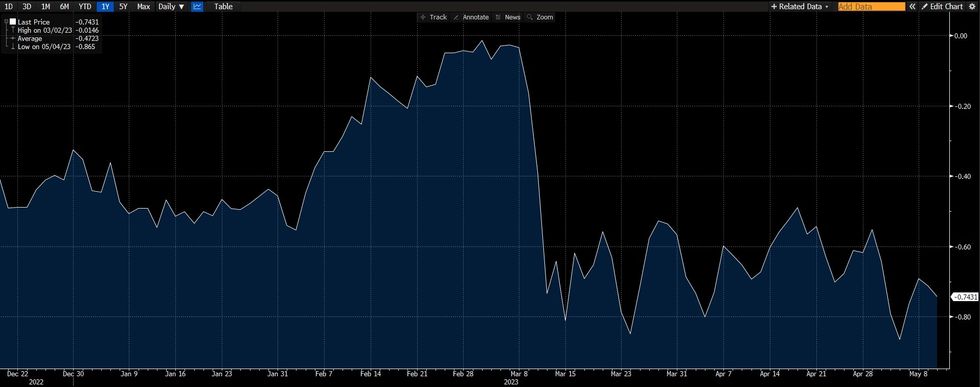

FOMC-dated OIS has eased on the back of some of the soft underlying CPI metrics that we have flagged previously (and will go over/reaffirm in CPI review), leaving only a couple of bp of tightening priced for next month’s meeting (3-4bp below pre-CPI levels), with a 25bp cut from terminal fully priced by September’s FOMC. Further out a cumulative ~75bp of cuts is priced by year-end (from terminal rate pricing) vs. sub-70bp of cuts being priced pre-data (remaining well within the established range). Note that 100bp of cuts from current terminal rate pricing is virtually fully priced come the end of the Fed’s Jan ’24 meeting.

- ING have noted that “If, as we fear, the combination of lagged effects of 500bp of Fed rate hikes and significantly reduced credit availability, as highlighted by the Fed’s Senior Loan Officers’ survey on Monday, do slow the economy sharply and unemployment starts to rise, the momentum will increasingly swing towards rate cuts. Right now markets are pricing a 25bp cut as soon as September. That may be a little early, but we think November and December are looking decent bets for the Fed moving policy to a more neutral setting.”

Fig. 1: FOMC-Dated OIS Jun ‘23/Dec ’23 Spread

Source: MNI - Market News

Source: MNI - Market News

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.