Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

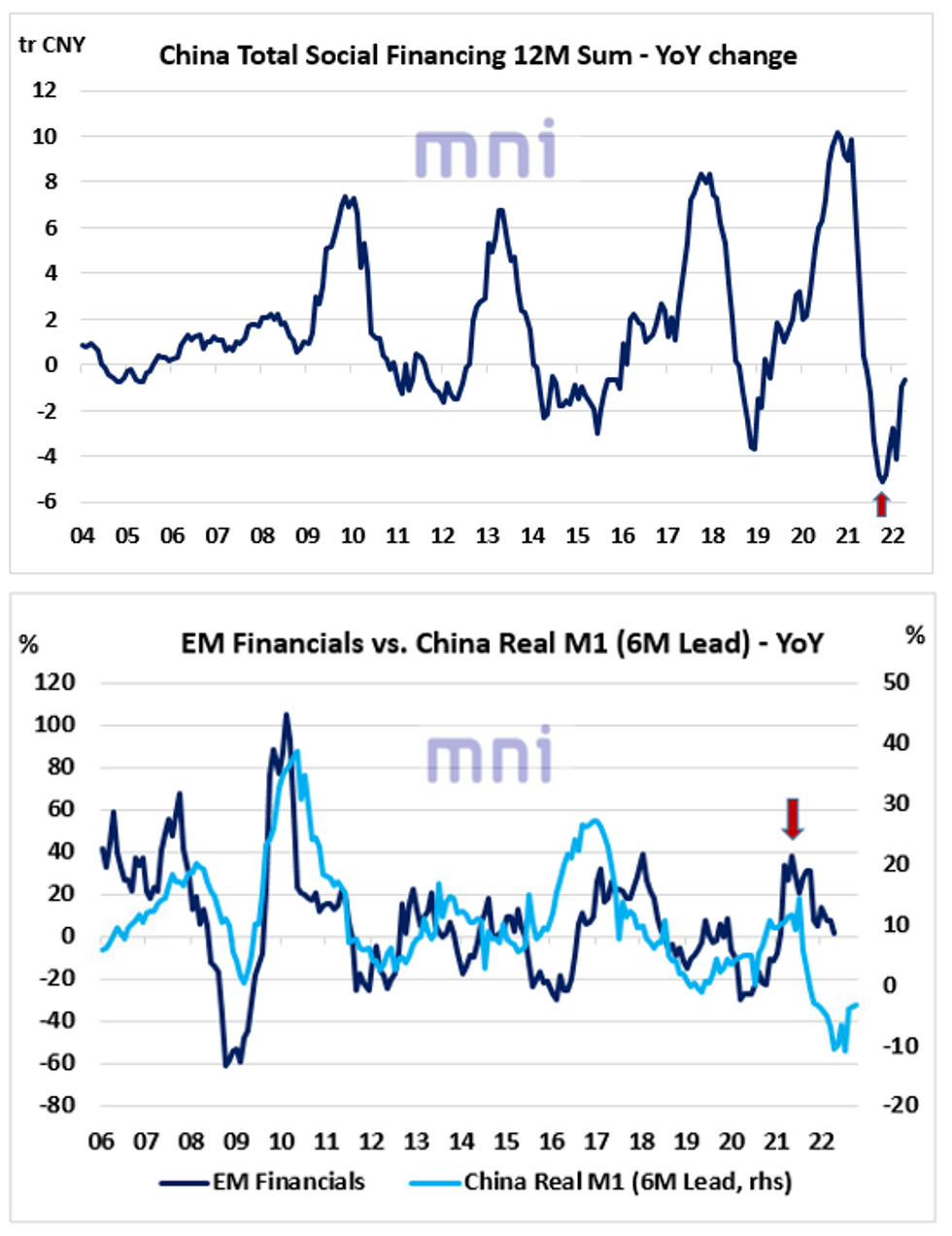

- PBoC reported on Friday that credit demand weakened sharply in April amid Covid lockdowns significantly disrupting the economic activity.

- Aggregate financing rose by 910.2bn CNY, significantly below expectations of 2.2tr CNY with new yuan loans rising by 645bn CNY (vs. 1.53bn CNY exp.).

- Even though the annual change in China Total Social Financing (TSF) 12M sum continues to rise (top chart), the disappointing ‘liquidity’ data could challenge domestic risky assets in the near term.

- The global risk off environment triggered by the renewed geopolitical tensions and surging stagflation risks have been weighing on Chinese equities in recent weeks.

- The Hang Seng index has been trading below the 20,000 level this week and is down over 20% since its early February high.

- China M1 money supply accelerated to 5.1% YoY in April (vs. 5% exp.), up from 4.7% the previous month.

- However, China real M1, which has historically acted as a strong leading indicator for cyclical equities (i.e. financials), is still standing at low levels historically and is currently pricing in further weakness in EM financial equities (bottom chart).

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok