Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

South Korean export growth was a touch above forecasts, up 5.1% y/y, versus 4.4% forecast, although still showed slowing sequential momentum from May (+11.5%). Still, the average daily export print came in at 12.4% y/y, versus 9% in May. Imports were weaker than forecast at -7.5%y/y (-4.7% projected and -2.0% prior). This aided a higher trade surplus, which printed just under $8bn for June ($5.7bn was forecast, prior $4.855bn). This is the highest surplus since Q3 2020.

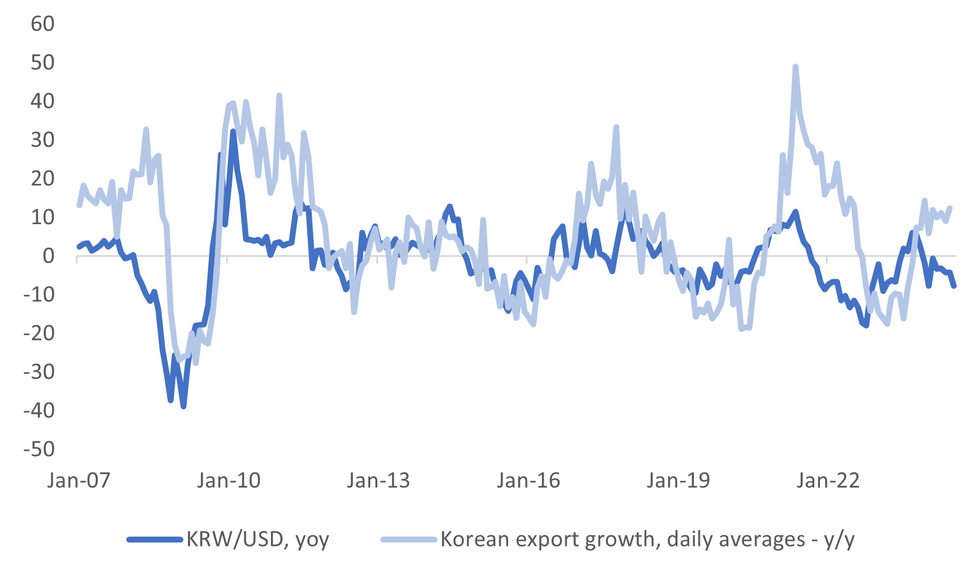

- The chart below overlays daily average export growth in y/y terms versus KRW/USD y/y changes. A modest divergence persists between the two series.

- Domestic capital outflow pressures, uncertainty around Fed easing and export growth concentrated in the tech/chip space have been highlighted as factors driving this wedge.

- Chips exports remained strong, +50% in y/y terms for June (recent cycle highs rest just above 60%). By country, exports to China were positive albeit just (+1.8% y/y). For the US it was +14.7% y/y.

- The lower import bill helped boost the trade surplus position. The trend on the trade surplus remains firmly positive, although the Citi South Korean terms of trade proxy is off earlier YTD highs.

Fig 1: South Korea Export Growth & KRW/USD Y/Y Changes

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok