Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK

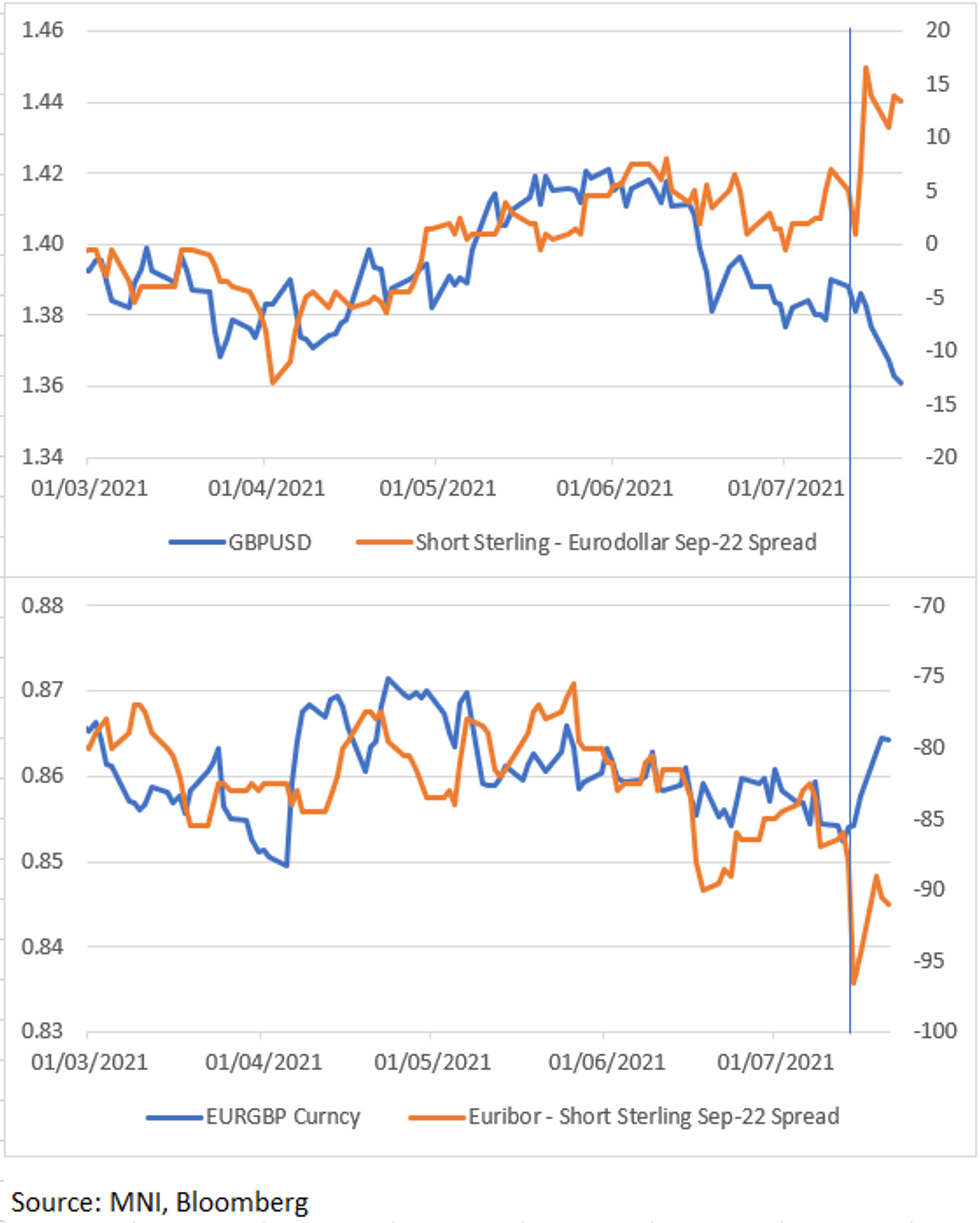

- Over the past 10 days or so the correlation between the pound and short-term interest rate markets has broken down.

- White (and to a lesser degree Red) Short Sterling futures markets have listened to the more hawkish comments from MPC members last week and are still pricing in a higher chance of rates hikes by the end of 2022 than they were last week ahead of the Cunliffe, Ramsden and Saunders comments.

- The pound, however, has been one of the losers of the risk-off move across global markets, with many putting the underlying reason for this as the spread of the Delta variant. If this is the reason, it makes sense for the pound to be underperforming as despite the high vaccination rate in the UK, cases of the delta variant are rising around 40% W/W and are around 50,000 per day.

- However, these views of the short sterling and the currency markets don't seem to square with each other.

- If we should be concerned about the delta variant in the UK, surely the market should then be ignoring hawkish commentary from MPC members as it would be unlikely that they would be able to tighten policy before the problems from the delta variant were more widespread.

- Alternatively, if the problem is a short-term problem for the UK then the moves in currency markets would look overdone.

- As the charts below show, the level of sterling weakness seems inconsistent with Sep-22 money market spreads against both the US and Eurozone and it appears as though at some point in the near future, money market and currency market views will need to converge.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok