Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CROSS ASSET

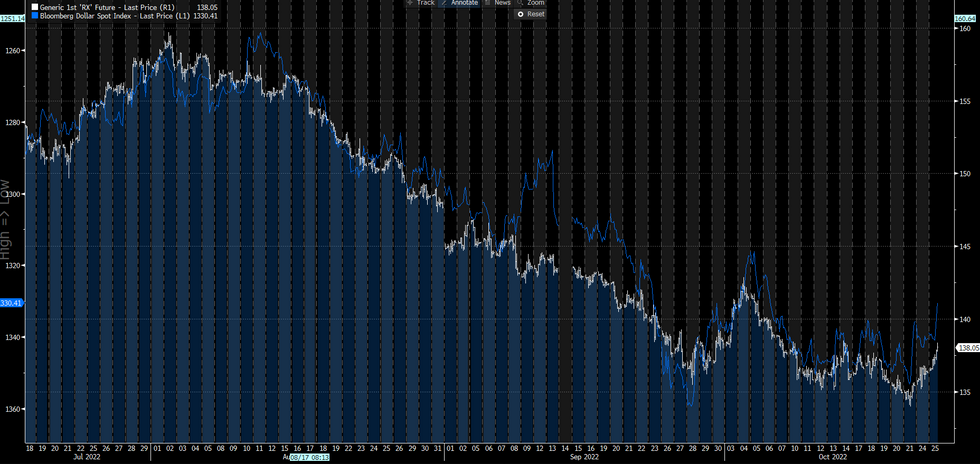

Further to our earlier note on Bund-USD correlations: periodically in the past couple of decades, EGB periphery spreads have appeared to drive EUR weakness/strength vs USD (2012-15); at other times, higher Bund yields relative to USTs have driven EUR strength vs USD (2008).

- In the current episode of high correlation over the past three months, Bund yields have actually been flat vs USTs (though the US advantage has gained sharply over the past 10 days), while BTP spreads have been fairly contained.

- But the US dollar's strength has helped pushing keep bond yields higher (and futures lower) as it transmits tighter Fed policy globally.

- To the extent that the Fed is seen holding back on tightening, it will give global central banks (including the ECB) room to set policy that may be more appropriate for their relatively weaker positions in the economic cycle without worrying about the imported inflation implications of a weaker currency.

- Indeed, despite talk of the recent dollar retracement being driven in part by speculation that the Fed will reconsider its hiking path, the Fed's terminal rate "advantage" has risen slightly today (Fed -6bp, ECB -9bp).

RX1 (Bund 1st Future) vs BBG Dollar Index (LH, Inverted)Source: BBG, MNI

RX1 (Bund 1st Future) vs BBG Dollar Index (LH, Inverted)Source: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok