Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

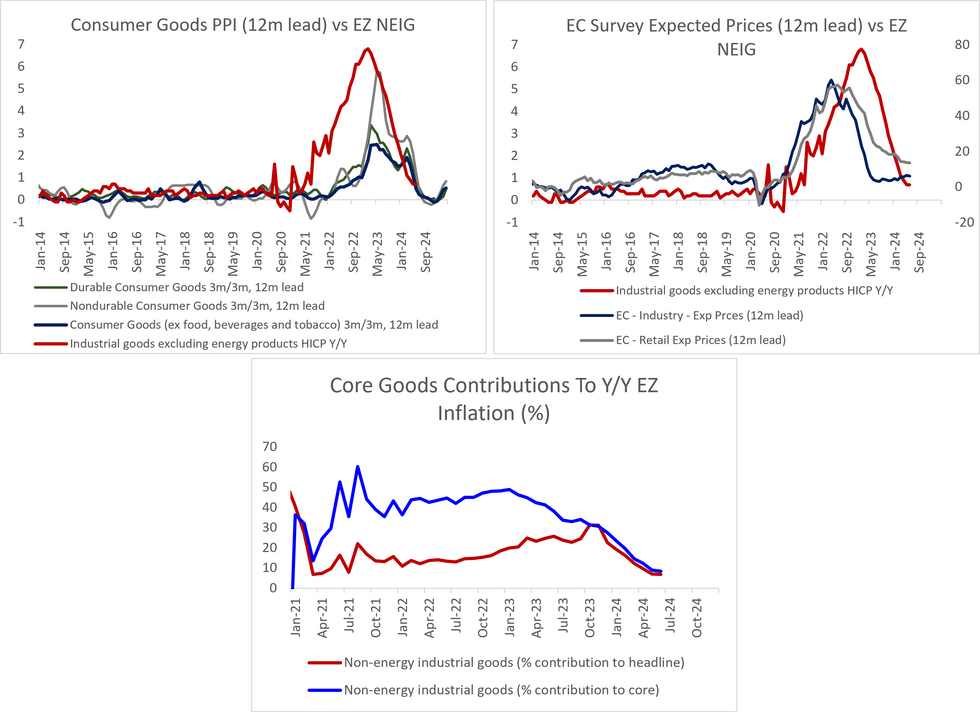

The July ECB meeting once again highlighted domestic price pressures (largely services) as the key source of upside risks to the inflation outlook.

- The (small) upward revisions to 2024/2025 Eurozone headline and core inflation forecasts in the June projection round included “only negligible impacts from geopolitical tensions in the Middle East (including disruption to Red Sea shipping) on goods inflation, consistent with shipping costs being a small share of total goods costs”.

- However, should core goods disinflation eventually stall and potentially start re-accelerating, the magnitude of disinflation required in other components (i.e. services) to achieve the 2% target increases.

- If services inflation remains sticky around 4% Y/Y and core goods inflation begins to re-accelerate in the coming months, this may pressure the ECB to make further upward inflation revisions in future projection rounds.

- This may also put upward pressure on EUR inflation swaps, which currently trade below the 2% target at 1- and 2-year ahead horizons.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok