Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

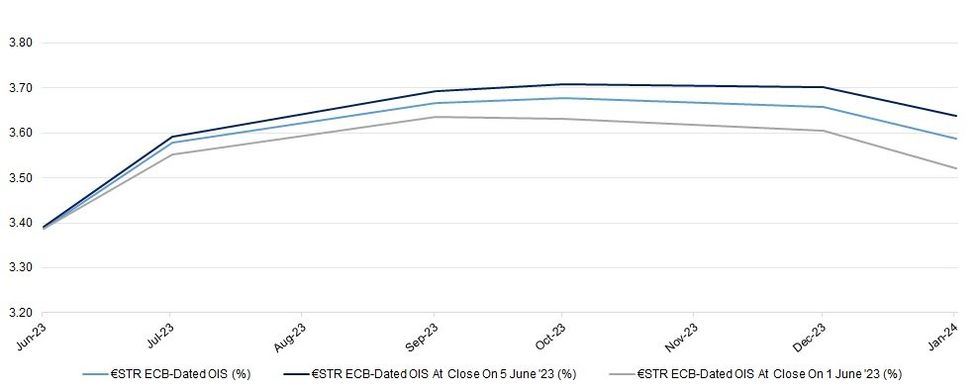

As noted earlier, the combination of lower crude oil prices (with yesterday’s lows comfortably breached) and the latest ECB consumer inflation expectations survey, revealing that “expectations decreased significantly - reversing most of the increases seen in the previous month,” have combined to pull ECB pricing lower today.

- That leaves terminal rate pricing in familiar territory, between 3.75-3.80% in deposit rate terms, with most of yesterday’s uptick eroded across the strip.

- Some pointed to comments from ECB hawk Knot, who noted that peak inflation was in the rear-view, although a closer look at his comments revealed continued worry that stickiness in inflation remains evident, with a hat tip to second-round effects becoming evident. Some caution re: potential corporate liquidity issues was also flagged, while Knot reaffirmed the idea that delayed impulses from already enacted tightening are still in the pipeline.

- Headline regional data releases (German factory orders and Eurozone retail sales) printed on the softer side of expectations.

- Looking ahead, ECB speak from Centeno & Vujcic will cross this afternoon. Note that the former speaks at a book presentation surrounding the topic of climate finance, while the latter has spoken on several occasions in recent days. That may limit the scope for meaningful market impact.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.388 | +24.0 |

| Jul-23 | 3.579 | +43.1 |

| Sep-23 | 3.667 | +51.9 |

| Oct-23 | 3.677 | +52.9 |

| Dec-23 | 3.658 | +51.0 |

| Jan-24 | 3.588 | +44.0 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok