Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

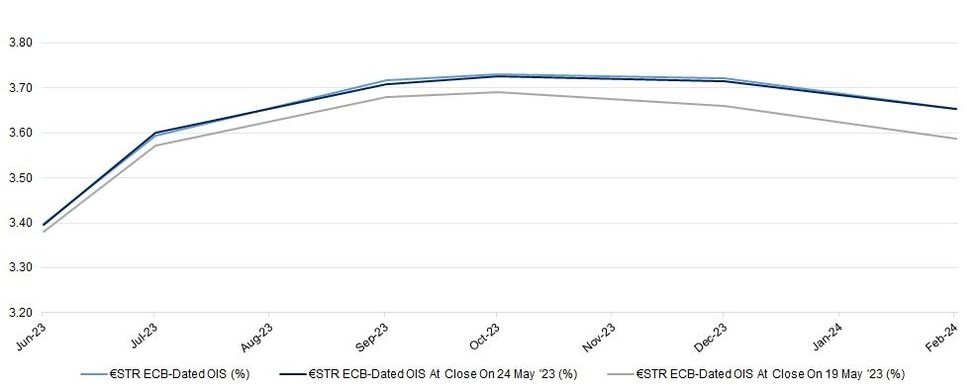

ECB-dated OIS is little changed to a touch firmer today, with terminal deposit rate pricing sitting at 3.85%, ~2.5bp firmer than May’s current closing highs (which were seen yesterday). 25bp of tightening is essentially fully priced for next month’s meeting, with terminal rate pricing now covering the October ECB gathering and a cumulative 60bp of hikes showing over that horizon.

- Today’s ECB speak has seen Vice President de Guindos outline the upside risks to inflation stemming from wages and profits, while flagging the downside risks rooted in banking sector headwinds, alongside expectations for inflation to decline rapidly. He also stressed that services inflation is the most worrying element of the core price pressure problem, along with a desire for governments to roll back some of the supportive measures surrounding energy prices.

- Bundesbank head Nagel pointed to the need to tighten further given the level of inflation.

- Bank of France Governor Villeroy once again stressed that further tightening is needed, along with highlighting the potential for delayed feedthrough into the economy given that rates are already “clearly in restrictive territory.” Villeroy went on to flag the need to reach terminal interest rate levels by the end of the Bank’s September meeting, while once again stressing that the bulk of rate hikes are in the rear-view.

- Meanwhile, Slovenian central bank chief Vasle reiterated the need for continued policy tightening, albeit at a slower pace.

- None of that has really moved the needle, with only de Cos left on today’s speaker slate.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.397 | +24.9 |

| Jul-23 | 3.598 | +45.0 |

| Sep-23 | 3.724 | +57.6 |

| Oct-23 | 3.748 | +60.0 |

| Dec-23 | 3.736 | +58.8 |

| Feb-24 | 3.677 | +52.9 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok