Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

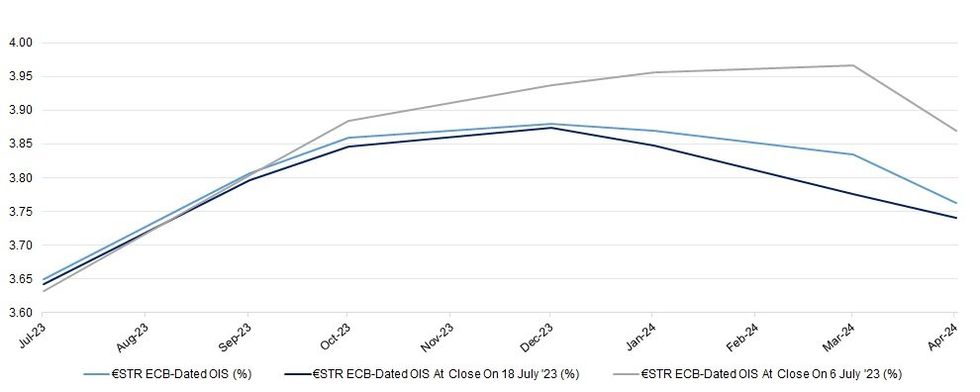

ECB-dated OIS is little changed to incrementally softer on the session, with the recent bid in core global FI markets and dovish BoJ sources pieces flagged elsewhere limiting any pay-side interest ahead of the weekend. That leaves a 25bp hike for next week’s meeting fully priced, with a cumulative ~40.5bp of tightening showing through September, while terminal deposit rate pricing operates just below 4.00%.

- These major markers respect the recent ranges after Governing Council hawk Knot provided a dovish impulse for markets earlier this week.

- BBG source reports recently indicated that “European Central Bank officials are anxious to strike the correct tone in describing their intentions after next week’s planned increase in interest rates” and that appears to be Madame Lagarde’s greatest challenge next week.

- Our full ECB preview will provide more details and colour ahead of the event.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jul-23 | 3.650 | +24.7 |

| Sep-23 | 3.807 | +40.4 |

| Oct-23 | 3.860 | +45.7 |

| Dec-23 | 3.880 | +47.7 |

| Jan-24 | 3.870 | +46.7 |

| Mar-24 | 3.835 | +43.2 |

| Apr-24 | 3.763 | +36.0 |

source: MNI Market News/Bloomberg

source: MNI Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok