Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

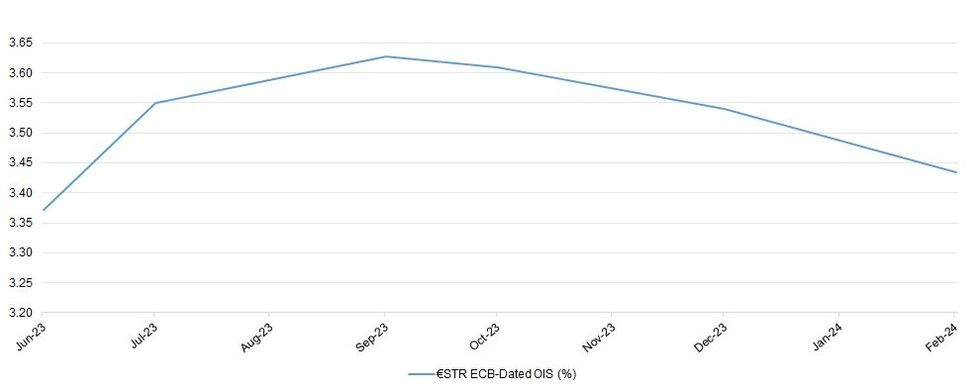

ECB-dated OIS sits little changed to incrementally lower, with terminal rate pricing hovering just shy of fully showing 2 further 25bp rate hikes. Meanwhile, just over 20bp of cuts is priced by the end of the Bank’s February ’24 meeting vs. current terminal rate pricing levels (which is seen come the end of the Bank’s September meeting).

- Early rhetoric from the head of the Greek central bank, Stournaras, stuck to his usual dovish lean. He noted that the current phase of ECB rate hikes is coming to an end, while highlighting the Bank’s data-dependent stance when assessing whether 1 or 2 further rate hikes will be required.

- This, coupled with some feedthrough from another run of softer than expected Chinese economic data has probably provided the modest downward pressure to pricing.

- ECB speak from President Lagarde & Vice President de Guindos is eyed today, with the potential for cross-market spill over surrounding U.S. data and a raft of Fedspeak also on the radar.

- This comes after the latest RTRS poll reiterated the well-trodden idea that the Bank “will hike its key interest rates by 25 basis points at each of the next two meetings, according to economists polled by Reuters, many of whom also said the bigger risk was rates could go higher still in the future.”

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.371 | +22.6 |

| Jul-23 | 3.551 | +40.6 |

| Sep-23 | 3.628 | +48.3 |

| Oct-23 | 3.609 | +46.4 |

| Dec-23 | 3.540 | +39.5 |

| Feb-24 | 3.434 | +28.9 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok