Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

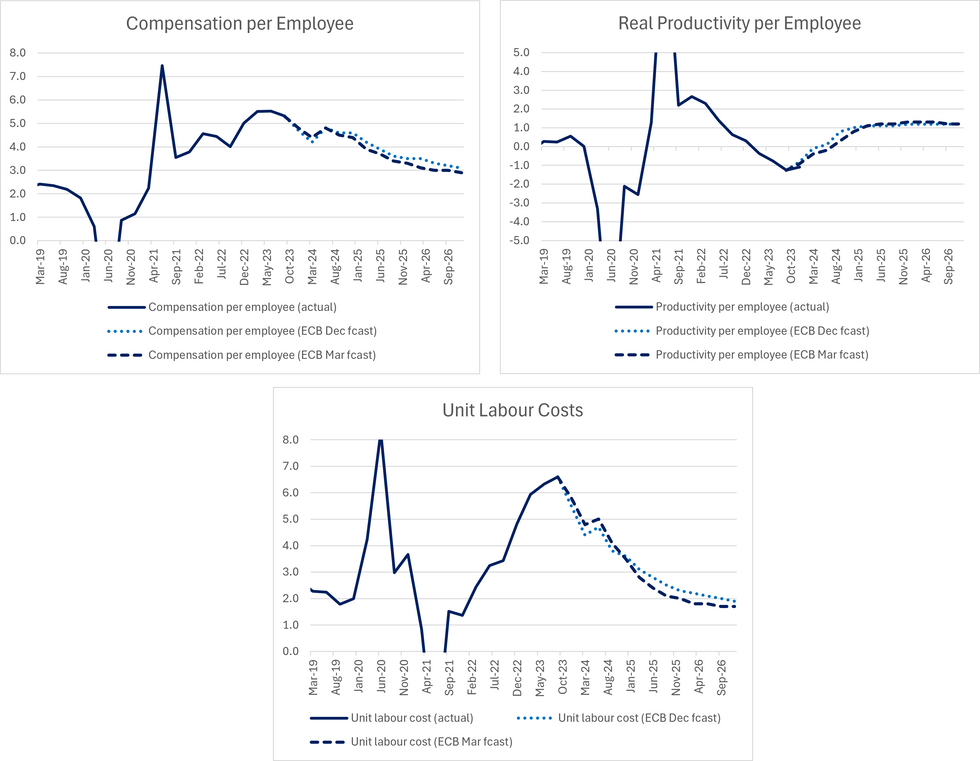

The ECB's updated macroeconomic projections provide a refreshed set of benchmarks to compare Q1 data against in the coming months. We note that ULCs appear to converge to equilibrium (around 2%) sooner than projected in December, potentially supporting earlier ECB cuts.

- President Lagarde once again stressed the importance of the Q1 national accounts data, much of which will only be available by the June ECB meeting, as an input into calibrating the policy easing cycle.

- Lagarde also reiterated the importance of the GDP deflator components - unit labour costs (ULCs) and unit profits - in understanding whether wage pressures are being buffered by profit margins. See our recent explainer piece here for more on that.

- Q1 2024 compensation per employee growth is seen at 4.4% Y/Y (vs 4.2% in the December projections). However, the overall profile of compensation has been revised lower across the forecast horizon (in 2024, because "lower wage drift owing to a weaker economic outlook is expected to more than offset stronger growth in negotiated wages").

- Real productivity has been revised lower through 2024, but is seen recovering through 2025 and 2026. The Q1 2024 forecast for real productivity per employee is -0.4% Y/Y (vs -0.1% in the December projections).

- Taken together, the ULC forecast for Q1 2024 is 4.8% Y/Y (vs 4.4% in the December projections). However, the 2025 and 2026 profile is lower than in December: "Growth in unit labour costs is expected to have peaked in 2023 and is projected to decline notably, benefiting in part from the projected rise in productivity growth".

- The Q1 2024 GDP deflator is forecast at 3.6% Y/Y (vs 3.3% prior). Across the forecast horizon: "Domestic price pressures, as measured by the growth of the GDP deflator, are projected to continue to decrease gradually with profit growth first providing a buffer for high labour cost pressure and subsequently recovering".

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok