Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

MNI (London)

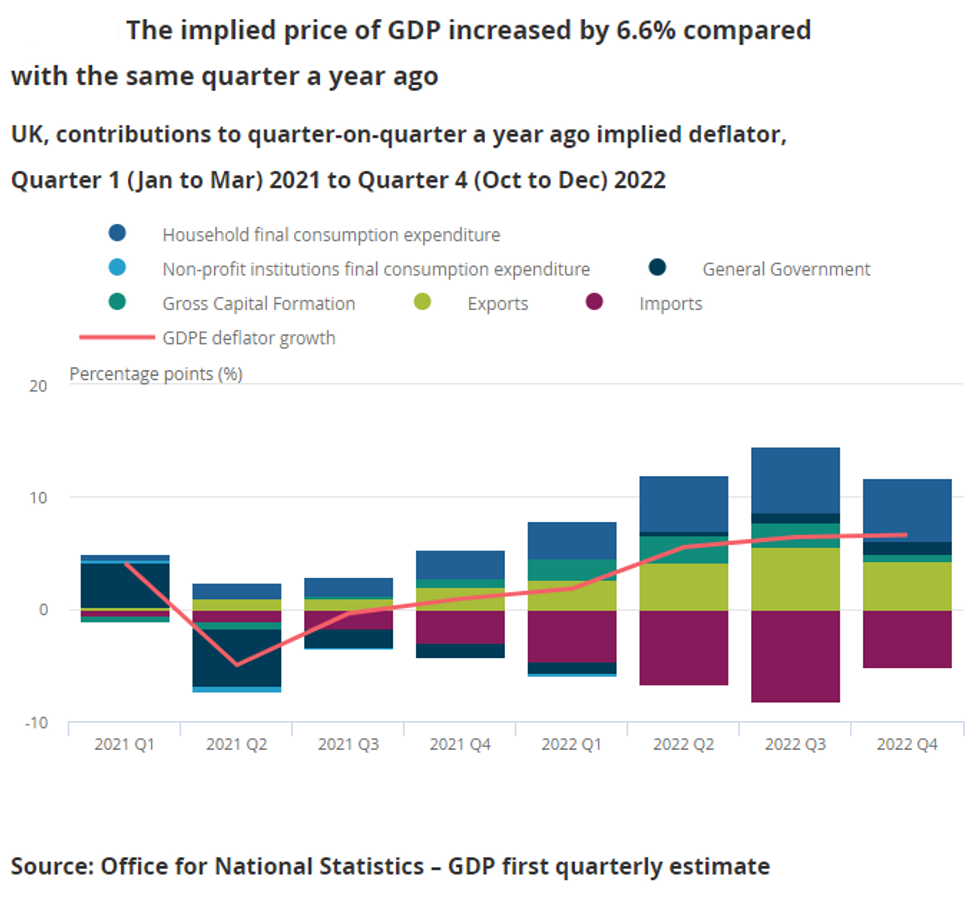

UK GDP contracted by -0.5% m/m, more sharply than anticipated, implying a flat Q4 GDP q/q reading (+0.01% q/q to 2dp) in line with expectations. Q4 2022 GDP was -0.8% below pre-pandemic Q2 2019 levels.

- Services largely accounted for the downside surprise in December, falling -0.8% m/m (vs -0.3% exp).

- Public services were hit by fewer operations and GP visits, lower school attendance and arts/entertainment (partly due to strike action). Meanwhile, hospitality slowed from the World Cup momentum.

- All up, services were flat on the quarter and private consumption recorded a minor +0.1% q/q, after contracting in Q3.

- In December, industrial and manufacturing production were more robust than forecast, at +0.3% m/m and 0.0% m/m after November contractions. Manufacturing was solely boosted by pharmaceuticals and transport, contracting elsewhere. Overall production declined by -0.2% q/q in Q4, driven by a fall in energy as consumers cut back usage.

- The trade gas prices increased substantially, driving the trade deficit wedge deeper to GBP -19.3B after -14.7B in November.

- All up, Q4 growth was marginally weaker than BOE forecasts but largely in line with expectations, with Q1 2023 expected to be negative. The BOE hinted that it needed data to outperform its modal forecast for more hikes to be needed. We didn't see that in the data today, but this won't stop a hike if we see upward surprises in wage, services CPI or inflation expectations data.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok