Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER STAPLES

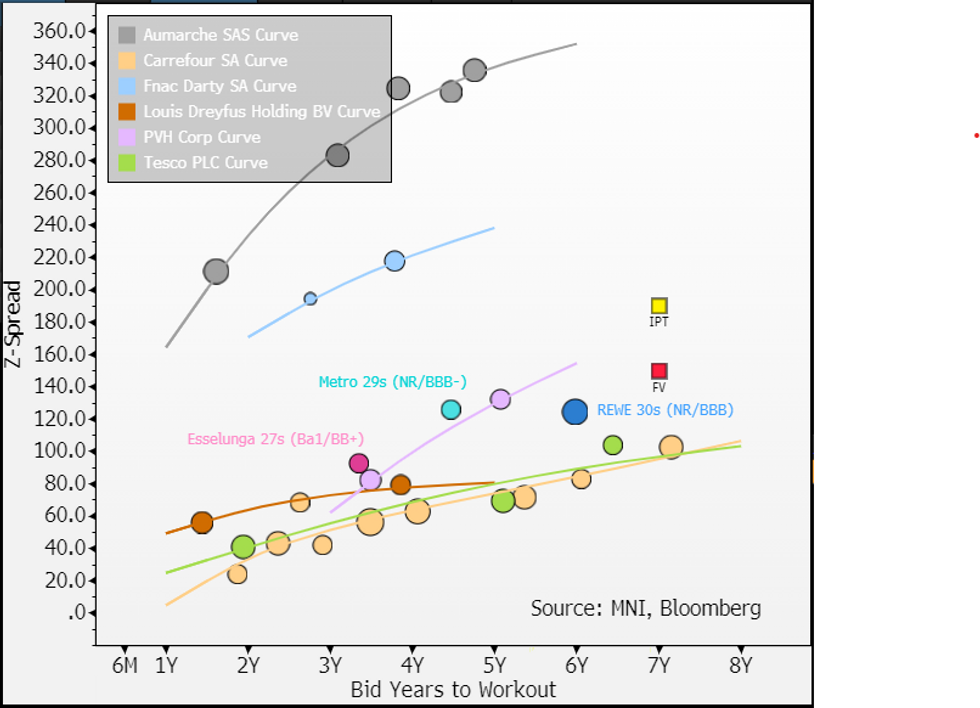

€500m 7Y IPT MS+190/200 vs. FV +150 (-40)

- We struggle to see value on this deal; FV is not far off our cheap view on 2y shorter & equal rated retailer PVH29s (Z+132). It trades well through our HY cheap view on French Elo/Auchan new 28s (Z+320) but on this name we advise investors wait out a expected rough 1H. Inside it we have a IG cheap view in grocers on Tesco31s at Z+104.

- Our FV is floored by German REWE 30's (REWEEG; NR/BBB) at Z+125. Its larger scale (€92.3b vs. €14.4b) and more diversified on 30% of sales outside Germany. Similar leverage (S&P adj. ~3x vs. 2.6x) and both are private co's.

- REWE30s are not dislocated - since issuance last year it has generally traded +40-50bps above French grocer Carrefour (NR/BBB).

- Cautions: we would have expected more of a discount for this deal - it is a private co and reporting looks annual (on website). Adding to that there was no mention of cash accounting (FCF/FOCF etc.) in the roadshow or on its website (we pulled figures from S&P). Though its diversified in what it does (apparel & food retailing/grocer/travel) it is not geographically (Spain) which we see as more limiting for RV views.

- "Aumarche" in below image is Elo/Auchan. Background on co here.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok