Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Turkey Central Bank

Executive Summary

- The CBRT is broadly expected to reduce its 1-wk repo by at least 100bp to 15.00%, but risks remain skewed towards a potentially larger cut.

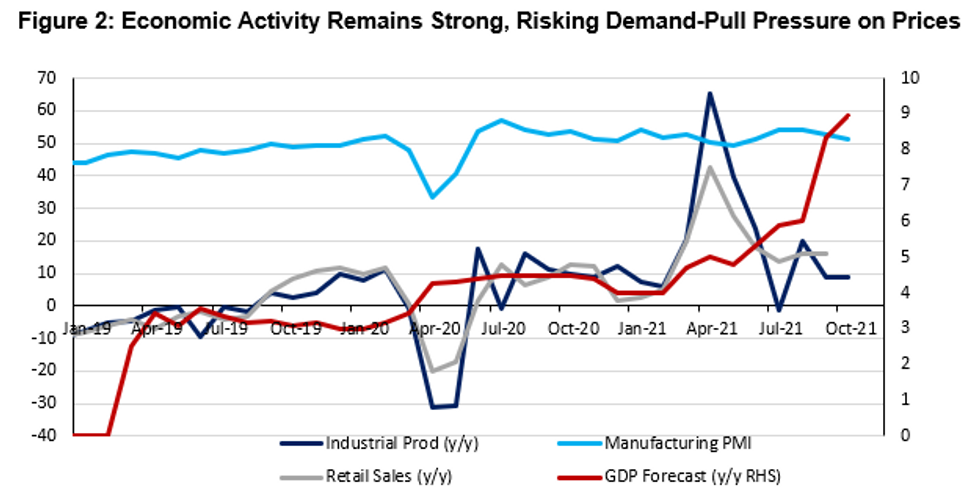

- Headline CPI & PPI continued to rise unabated in October, while core metrics (CBRT benchmark) marked a small decline to 16.82% from 16.98% - reinforcing the CBRT's easing bias broadly against the trend of tighter policy in EM.

- Higher FX passthrough and dollarisation continue to create a vicious circle of snowballing risks to inflation and further TRY depreciation pointing to a concerning longer-term outlook

- Uncertainty around CBRT policy remains high, with the Bank's reaction function reflecting more dominant political decision-making drivers than market-based - creating scope for more near-term TRY volatility.

Full Preview Here:

The CBRT is broadly expected to reduce its one-week repo rate by at least 100bps to 15.00% as the bank resumes its easing cycle against the EM trend. Here, we see the majority of analysts taking Kavcioglu's guidance on limited room to cut rates at face value, justifying the relatively smaller cut relative to the 200bps shed last month. However, with the bank's reaction function being less dictated by market conditions than political vectors, risks are unequivocally skewed towards a potentially larger cut.

MNI London Bureau | +44 020-3983-7894 | murray.nichol@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok