Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

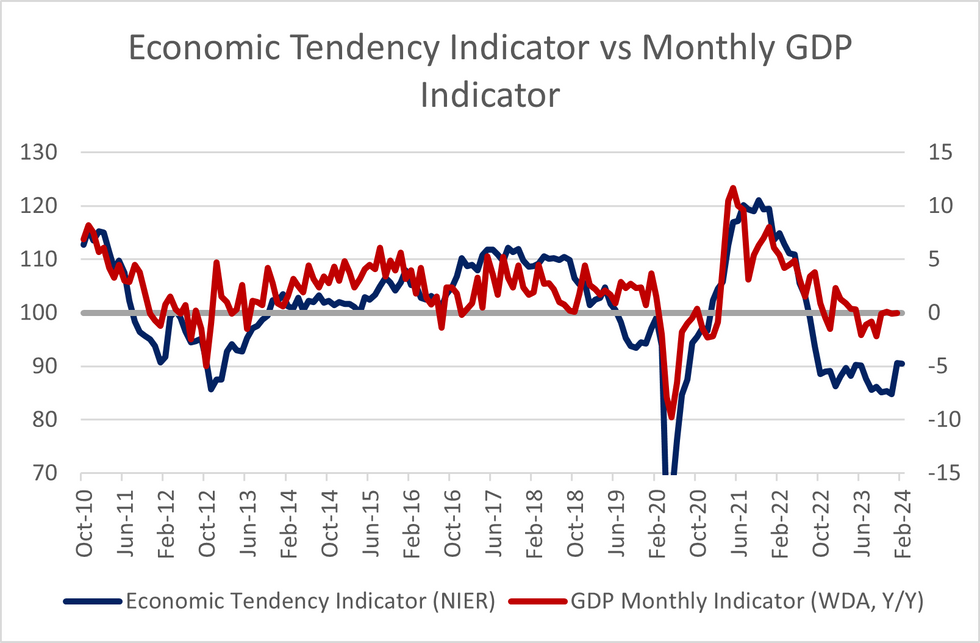

Business pricing plans in the February Economic Tendency Indicator took a marked step lower compared to levels seen in January and much of the last 2 years. This will be very encouraging for the Riksbank, and provides support to those looking for a H1 2024 rate cut.

- Across industries, expected selling prices fell to 14 from 20 in January, the lowest reading since March 2021. This trend was seen across services, manufacturing and retail trade. The release notes that "pricing plans are only just above the historical average".

- The overall Economic Tendency Indicator was broadly steady at 90.5 (vs an upwardly revised 90.6 prior). The industry sub-components mostly saw minor changes to January (+/- 1 point) with the exception of the building/civil engineering sector (94.7 vs 91.3 prior - the improvement due to "less negative employment plans).

- Overall, sentiment remains below the neutral 100 level in all sectors.

- Employment expectations across industry overall were neutral (at 0, vs +1 in Jan and -3 in Dec), while the labour hoarding indicator was steady vs January.

- Consumer confidence remains below the "much weaker than usual" 90 handle, printing at 82.7 (vs an upwardly revised 82.7 in January). It is nonetheless encouraging that January's rise to to 82.7 (after 75.1 in December) was not reversed.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok