Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE DATA

French inflation came in above expectations in August's flash reading: headline CPI at a 3-month high 4.8% Y/Y (vs 4.6% survey) was an acceleration from 4.3% in July, while the HICP headline rate of 5.7% (vs 5.4% survey) quickened from 5.1% prior.

- On a sequential M/M non seasonally adjusted basis, CPI accelerated to 1.0% (0.8% survey), the joint-fastest since March 2022, from 0.1% in July with HICP up 1.1%, joint-fastest since Oct 2022 (1.0% survey), vs 0.0% prior.

- Looking into the details though, core prices looked to have decelerated in August from July's 4.3% Y/Y in HICP - though INSEE does not publish a flash estimate.

- A rise in energy prices (+6.8% Y/Y vs -3.7% in July) - which had been anticipated on the back of higher oil prices and higher regulated electricity prices - was responsible for much of the acceleration, with most other categories steady / decelerating.

- That included food (11.1% Y/Y vs 12.7% Jul), tobacco (9.9% vs 9.8% Jul), manufactured goods (3.1% vs 3.4% Jul), and services (2.9% vs 3.1% Jul).

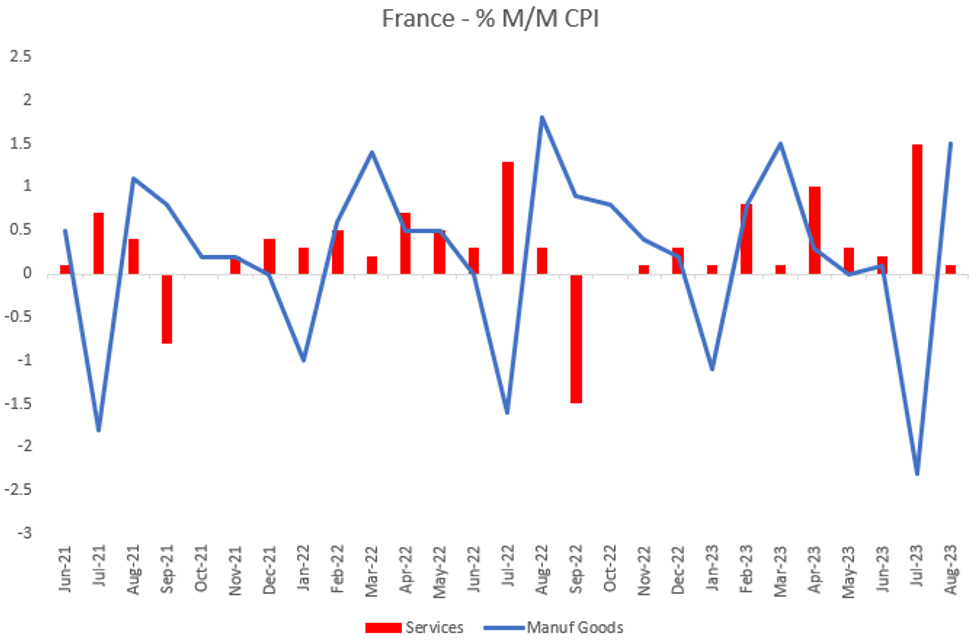

- On services, INSEE note a downturn in transport and "other service" prices keeping a lid on overall services, which rose 0.1% M/M sequentially after a series record 1.5% in July; manufactured goods were up 1.5% vs -2.3% in July (which had been negatively impacted by an extended sales period).

- Overall, core goods look to have been relatively subdued after a volatile July: Services 0.1% ran at a rate below the 0.2% average for Augusts in the previous decade, suggesting July's jump was a one-off, and goods prices have averaged -0.2% M/M the past 3 months.

Source: INSEE, MNI

Source: INSEE, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok