Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

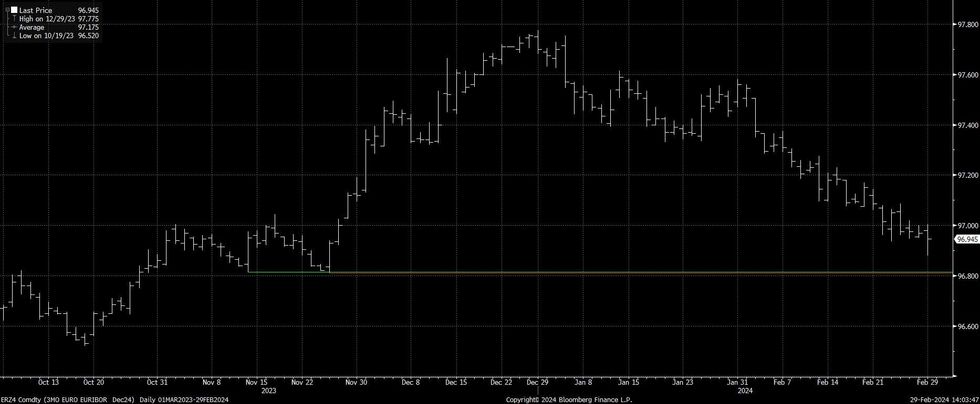

EURIBOR

ERZ4 futures have fallen by ~65bp in February.

- ECB-dated OIS shows 85-90bp of cuts during ‘24.

- Those that believe the ECB will deliver more cuts than the market prices may look to start scaling into long ERZ4 positions if the contract moves 10-15bp lower (ahead of 75bp of cuts being priced for '24).

- On top of this, technical support is seen at the Nov ’23 double bottom (96.810/815).

- June '24 seems like the preferred ECB meeting to start the cutting cycle at present .

- Assuming the ECB does implement its first 25bp rate cut in June, it would have to cut rates by 25bp at 2/4 remaining ’24 meetings to achieve 75bp of cuts this year.

- Our policy team’s most recent sources piece suggested that GC members see a range of 50-100bp of cuts in ’24, with 75bp obviously falling in the middle of that range.

- Risks to any potential long Euribor positions include momentum, which has been notable since late Nov.

- Furthermore, the dovish Governor of the Maltese central bank (who is open to a March ’24 cut) recently told us that that a majority of the ECB GC remains sceptical that inflation has come down quickly enough to justify easing policy.

- That, coupled with the need to keep financial conditions tight enough, suggests that hawkish risks will remain until another move lower in inflation is seen.

Fig. 1: Euribor December ’24 Futures (ERZ4)

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok