Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CREDIT MACRO

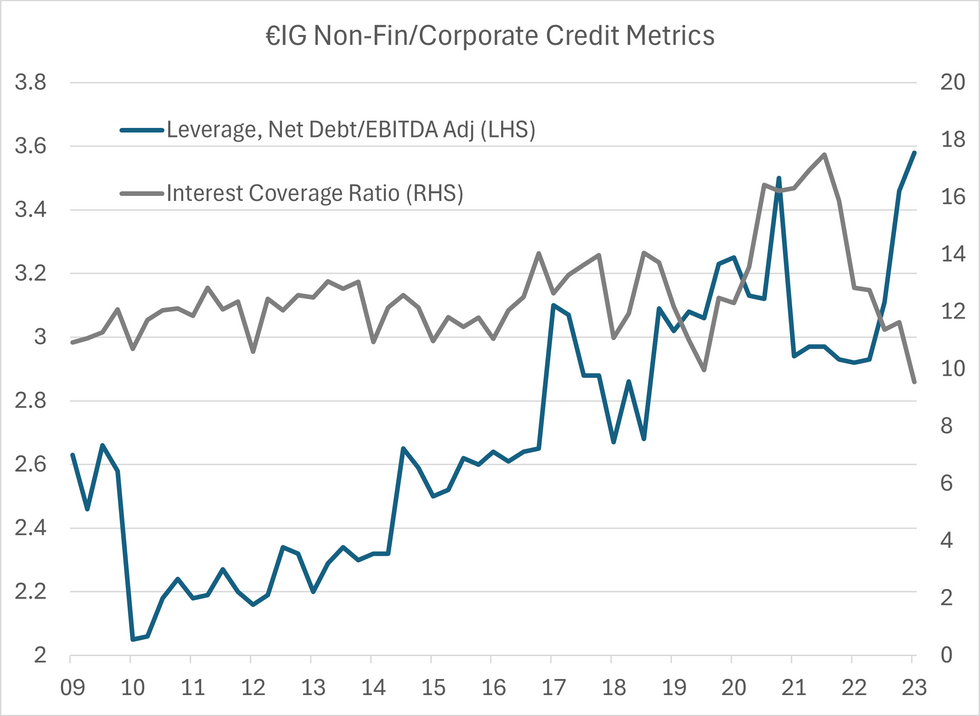

Credit metrics on Bloomberg Indices for Q4; €IG* Leverage for €IG corp's were little changed at 3.6* (vs. 3.5* last qtr).

- Only notable sector was consumer cyclicals that de-levered from 3.8* to 3* (now at levels from 1Q22).

- Coverage ratios fell by 2* to 9.6*.

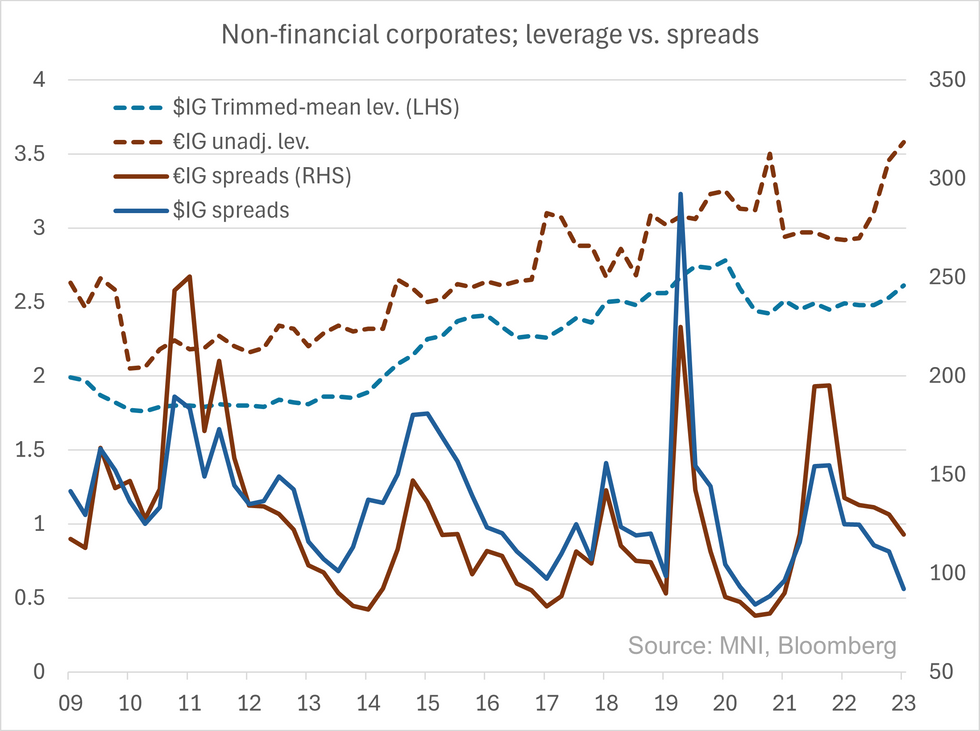

- Against $IG reported metrics (which are a tad cleaner given trimmed means vs. unadjusted for us) we do look worse given at historic peaks.

- Hard to translate that directly to spreads - avg. cash price on both indices has moved in tandem (to ~93) but we've had vol in index maturity/duration - initially higher during Covid/rate cuts & now lower to 5.5/12.5yrs - hence cautions delving too far into cross-currency cash index comparisons.

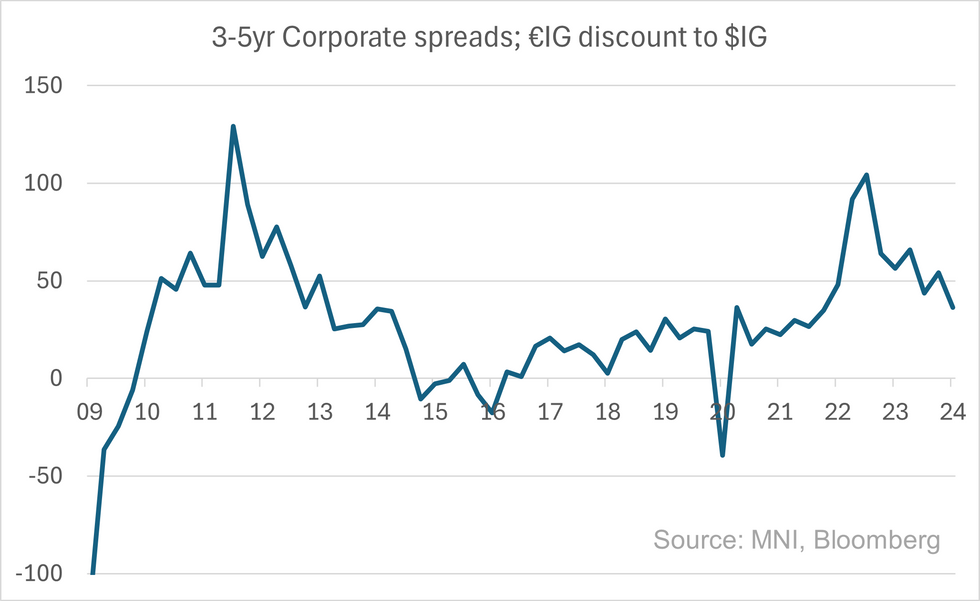

- On Equal tenor (3-5yr) comparisons (below) we see €IG trading even more wider to $IG (vs. historical).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok