Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

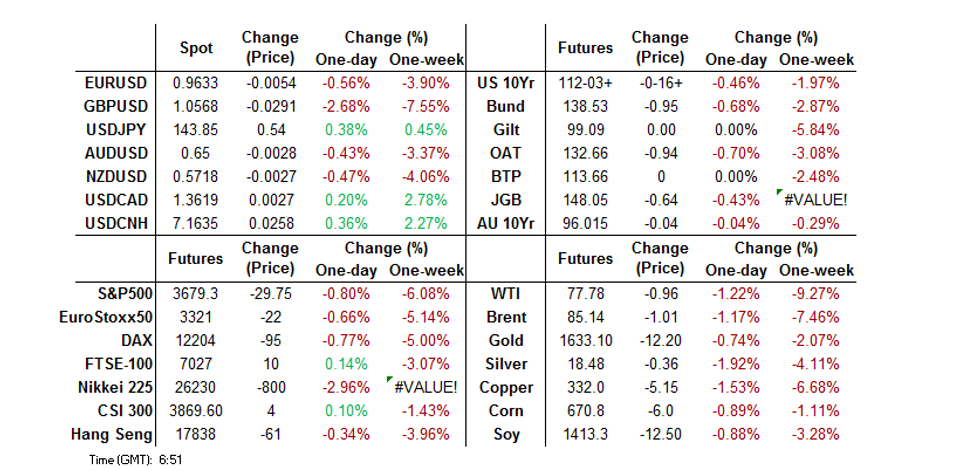

- Global core FI markets struggled in Asia, with the prospect of further fiscal easing from the UK and the victory of the centre-right coalition in the Italian election, alongside the inability of that faction to secure a super majority (the most market “unfriendly” outcome), combining.

- Aggressive sterling sales resumed Monday morning as PM Truss' government stood by its mini-budget which inspired sharp depreciation in the exchange rate last Friday. In the weekend round of interviews, Chancellor Kwarteng played down the initial market reaction to his fiscal plans and doubled down on his pledge to cut taxes and boost spending, while refusing to commit to any limit on borrowing. USD/CNH hit a fresh high of just under 7.1740, despite another stronger CNY fix and a hike in the forward FX reserve level for banks

- The central bank speaker slate is tightly packed today. President Lagarde headlines a parade of ECB members, while comments are also due from Fed's Bostic, Mester & Logan, as well as BoE's Tenreyro & BoJ's Kuroda. German Ifo survey takes focus on the data front.

US TSYS: Weaker On UK Fiscal & Italian Political Mix

TYZ2 prints around the base of its 0-18+ overnight range into London hours, on volume of ~115K. Cash Tsys sit 4-7.5bp cheaper, with intermediates leading the weakness.

- Regional reaction to Friday’s Gilt-driven weakness in core global FI markets and the prospect of further fiscal support in the UK applied pressure during the early rounds of Asia-Pac dealing.

- The victory of the centre-right coalition in the Italian election, alongside the inability of that faction to secure a super majority (the most market “unfriendly” outcome), added further pressure.

- 2- & 3-Year yields have registered fresh cycle highs after the previous extremes limited weakness in the space earlier in the day.

- The 5-/30-Year yield spread has printed a fresh cycle low, while the 2-/10-Year yield curve is little changed, hovering a little above its own cycle extremes (J.P.Morgan have recommended initiating 2-/10-Year flatteners).

- Flow was headlined by a block sale of FV futures (-10K) and block buy of the TYX2 110.00/114.00 strangle (+10K).

- Dallas & Chicago Fed activity data, 2-Year Tsy supply and Fedspeak from Mester, Bostic, Collins & Logan headline domestic matters on Monday.

- Gilt reaction to fiscal-related weekend rhetoric and any European reaction to the Italian election will be eyed in pre-NY dealing.

JGBS: Curve Steeper, Futures Not Challenging Recent Base

Futures print -63 heading towards the Tokyo close, with the bulk of the movement coming during the early rounds of Tokyo trade.

- Last week’s low (147.94) in the contract wasn’t tested and continues to provide initial technical support.

- Cash JGB trade saw the major benchmarks run 1.0-7.0bp cheaper, with 10-Year yields being capped by the upper limit of the BoJ’s YCC mechanism (promoting curve steepening).

- Wider FI market weakness pressured JGBs after Tokyo returned from a long weekend.

- 20s and 40s have registered fresh cycle highs (in yield terms) on the move.

- Familiar language was deployed by Japanese Finance Minister Suzuki, which failed to impact JPY, as you would expect.

- Offer/cover levels remain contained in the BoJ’s 1- to 10-Year Rinban operations, even with 10-Year yields challenging the upper limit of the BoJ’s YCC, suggesting a lack of meaningful desire to test the BoJ’s will at present.

- BoJ Governor Kuroda will speak shortly, but we don’t expect much new, owing to the proximity to last week’s monetary policy decision & subsequent press conference.

- Further out, 40-Year JGB supply headlines domestic matters tomorrow, with services PPI & machine tool orders data also due.

AUSSIE BONDS: Holding Flatter, OIS Moves Higher Again

Aussie bond futures have stuck to relatively tight ranges during Sydney dealing, failing to probe their respective overnight session bases, leaving YM -9.5 and XM -3.0 as we move towards the Sydney close.

- Wider cash ACGB trade sees the major benchmarks running 9bp cheaper to little changed, with the flattening impetus maintained through the session.

- Bills run 8-18bp cheaper through the reds, with RBA dated OIS adjusting higher in early Sydney trading.

- OIS now price ~45bp of tightening for next month’s RBA, while terminal rate expectations sit at ~4.30%, a little shy of session highs, but still ~15bp firmer on the day.

- The 3-/10-Year EFP box has flattened, with payside flows/hedging linked to the aforementioned OIS repricing likely helping 3-Year EFP push ~6bp wider, while 10-Year EFP is ~1bp wider.

- The lack of meaningful domestic headline flow and scope of the moves in core global FI markets left broader drivers at the fore.

- Tomorrow’s domestic docket is slim, with I/L supply from the AOFM the only point of note.

FOREX: UK Fiscal Outlook Sends Cable To Record Lows, PBOC Slaps 20% Risk RRR On FX Forward Sales

Aggressive sterling sales resumed Monday morning as PM Truss' government stood by its mini-budget which inspired sharp depreciation in the exchange rate last Friday. In the weekend round of interviews, Chancellor Kwarteng played down the initial market reaction to his fiscal plans and doubled down on his pledge to cut taxes and boost spending, while refusing to commit to any limit on borrowing.

- The Telegraph reported that Truss could face a rebellion from Tory backbenchers if cable falls to parity, while the pound's sharp depreciation has raised questions about the likelihood of BoE action to rescue the beleaguered currency.

- GBP/USD tumbled to an all-time low of $1.0350 before stabilising near the $1.0500 mark in a volatile session. Implied volatilities were sharply higher across the maturity curve, with one-month tenor printing best levels since the outbreak of the COVID-19 pandemic.

- EUR/GBP surged to its highest point since Sep 2020, taking out the GBP0.9100 figure in the process. The single currency showed little in the way of outright reaction to the preliminary results of Italy's general election, with the right-wing bloc on track for an absolute majority.

- Sterling weakness underpinned USD outperformance as the BBDXY index advanced to a new record high of 1,355. The greenback drew additional support from higher U.S. Tsy yields as cash trading resumed in Tokyo after Japan's long weekend.

- USD strength pushed USD/JPY towards the Y144.00 mark, even as Japanese officials rattled the intervention sabre. FinMin Suzuki expressed concern about "speculative moves" and vowed readiness to step in if needed.

- Offshore yuan got some brief reprieve as the PBOC slapped a 20% risk reserve requirement on FX forward sales, but spot USD/CNH promptly resumed its uptrend, with the USD/CNY mid-point set above CNY7.0 for the first time since 2020.

- The central bank speaker slate is tightly packed today. President Lagarde headlines a parade of ECB members, while comments are also due from Fed's Bostic, Mester & Logan, as well as BoE's Tenreyro & BoJ's Kuroda. German Ifo survey takes focus on the data front.

FOREX OPTIONS: Expiries for Sep26 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9700-20(E701mln), $0.9800(E594mln), $0.9900-10(E1.7bln), $1.0000-20(E563mln)

- USD/JPY: Y140.00($1.0bln)

- GBP/USD: $1.1500(Gbp513mln)

- AUD/USD: $0.6550(A$966mln)

- USD/CAD: C$1.3600($704mln)

ASIA FX: Little Relief For CNH Despite Fresh Policy Support

The USD has continued to rally against Asian FX, albeit to varying degrees. CNH has weakened to fresh cyclical lows, likewise for KRW, TWD, and SGD, while INR has made another fresh record low. Tomorrow China industrial profits for August are due, along with South Korean consumer confidence. Neither release is expected to shift sentiment.

- USD/CNH hit a fresh high of just under 7.1740, despite another stronger CNY fix and a hike in the forward FX reserve level for banks. We are back now at 7.1690, but dips remain supported. Previous highs just under 7.2000 are being eyed.

- Spot USD/KRW is at 1433, 1.65% above last Friday's close. Onshore equities have fallen sharply, down 3%. BoK Governor Rhee spoke to the local parliament but hasn't shifted sentiment a great deal.

- USD/TWD is up above 31.87, a fresh cyclical high. Local stocks are down 2.50%, led by the tech sensitive sector.

- USD/SGD is above 1.4350, fresh highs back to early 2020. The currency is outperforming broader USD gains. The SGD NEER is higher in the session. IP growth for August was better than expected at +2.0 m/m (1.5% expected).

- USD/IDR has turned bid, absorbing risk-off flows, with the pair +87.50 figs to 15125 last. Weaker commodity prices are weighing, while there is little of real note on the local data docket this week.

- USD/INR has pushed through 81.55, to a fresh record high. Onshore equities are struggling, down over 1.6% so far in trade. This Friday the RBI decision is due, where the central bank is expected to raise rates by 50bps (to 5.90%).

- Spot USD/MYR has appreciated in line with a surge in the broader dollar. We were last just shy of 4.6000. Topside technical focus falls on MYR4.6100, which capped gains twice in January 1998.

MARKET INSIGHT: CNH: Hiking FX Forward Reserve Requirements May Not Prevent Fresh Lows

Neither USD/CNH, nor onshore USD/CNY spot, has seen much follow through post the PBoC's announcement that it will raise the risk requirement on banks' forward FX sales to 20% (from 0%). The move is designed to make it more expensive to short the yuan in the forward space.

- USD/CNH dipped sharply towards 7.1300, but we now sit back close to 7.1600, just below earlier highs close to 7.1650. Onshore spot has pushed higher as well (near 7.1600). We are close to the top end of today's trading band (-/+ 2% above the USD/CNY fix), which comes in at 7.1704.

- Today's move arguably hasn't surprised the market too much given the recent pace of depreciation pressures and getting close to previous highs (close to 7.2000). We also noted on Friday, risks of fresh FX policy action were rising, (see this link for more details).

- Changing reserve requirement on forward transactions was first introduced in September 2015, post the devaluation. It was removed in 2017, before being reinstated in 2018 (during the US-China trade conflict), then removed in 2020.

- In both 2015 and 2018, hiking of the forward FX reserve rate didn't prevent fresh cyclical lows in the currency over multi-week horizons post the announcement.

- These previous episodes were also more China centric in the sense the 2015 period was focused on deleveraging offshore liabilities, while in 2018, it was the trade conflict.

- This time around CNH is more a victim of broad based USD strength, although policy differentials (as signified by the very negative level of CNH forward points) and a much weaker growth back drop aren’t helping either. Hence today's announcement may not be enough to prevent fresh cyclical highs in USD/CNH.

EQUITIES: Growth Sensitive Equities Falter

Outside of China and Hong Kong, broader equity market sentiment has been weak. US futures are in the red (-0.60%), with negative spill-over from a stronger USD (particularly against GBP) evident in the equity space today. The risk averse tone from late last week has persisted, particularly in relation to growth sensitive stocks (tech/commodities).

- The HSI is in positive territory (last +0.17%), with tech shares (+2.33%) jumping, albeit from very depressed levels, while Macau casinos are up on a report mainland tours could resume as soon as November.

- Mainland China shares are also trading resiliently. Early impetus came from property developers after a report that China Construction Bank will buy assets off developers. However, we are now away from best levels, while the aggregate Shanghai composite index is down smalls.

- Growth/rate sensitive markets in South Korea and Taiwan have faltered. The Kospi is off by around 3%, the Taiex -2.25%.

- Australian shares are down by around 1.35%, with mining related stocks seeing the sharpest falls.

GOLD: Fresh Lows Back To 2020

Gold has seen little support today, despite fresh risk aversion flows in the market. The precious metal last tracked just under $1639 (-0.30% for the session). On-going USD strength, particularly against the pound, has been the main driver of sentiment today.

- We dipped below $1630 briefly in earlier trade today, before rebounding. We have since not drifted too far away from the $1638/$1642 region, although the bias remains skewed to the downside.

- Lows close to $1600 from early April 2020 around $1610 are the likely next target.

- We continue to see higher core yields. To the extent this weighs on broader equity market sentiment further could benefit gold at some stage but with this could be countered by further on-going USD strength.

OIL: Can't Escape Broader Risk Aversion/Demand Concerns

Brent crude's earlier spike above $87/bbl quickly gave way to fresh selling pressure. There is still support evident around $85.50 though, with crude not dipping below this support level, which was also evident through the Friday offshore session as well. We last tracked just above this level at $86.65. WTI is around $78.30 currently, displaying similar trends.

- Oil headwinds continue to persist from the broader demand standpoint, particularly as major central banks tighten policy to curb inflation pressures, which is taking precedence over any growth concerns.

- On the supply front, Iran looks boost capacity to 5.7mn barrels per day over the medium term and is seeking outside investment even without a fresh nuclear deal with the US.

- Elsewhere though, at the Singapore Asia Pac Petroleum Conference, the focus is on OPEC+ supply and when the organization might respond to weaker demand conditions as we move into Q4.

- There is also a tropical storm off the coast of Florida, which will be eyed for potential supply disruptions later in the week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.