Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

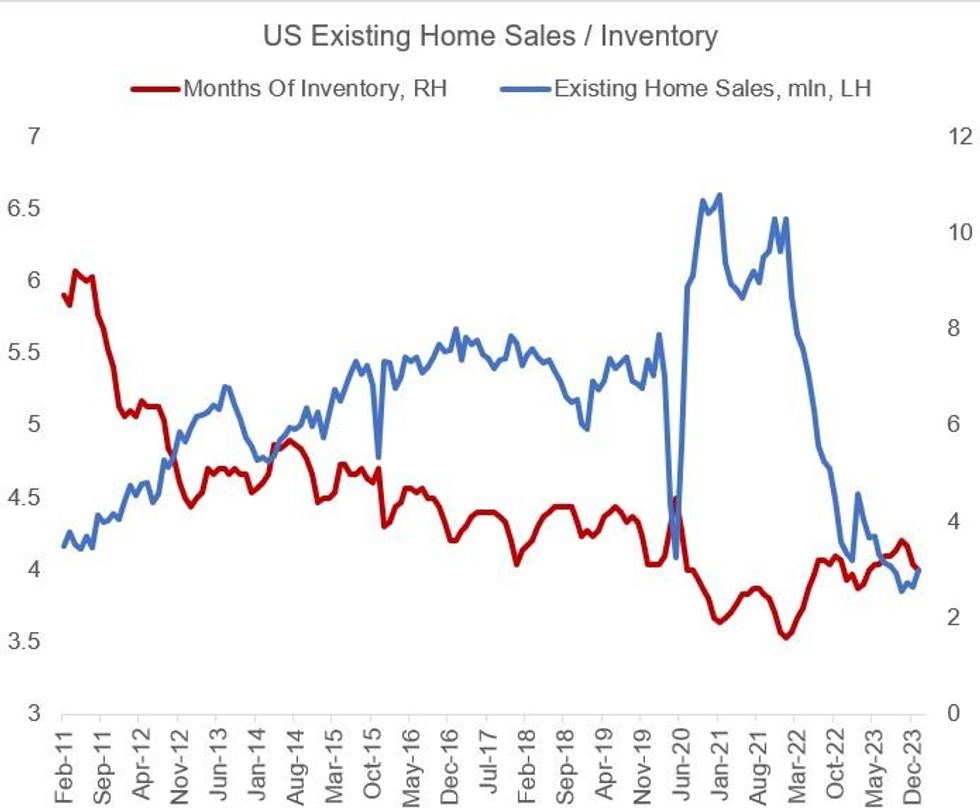

January existing home sales were roughly as expected, at 4.00mln (SAAR), vs 3.97mln expected and a 3.1% gain vs 3.88mln in December (upwardly revised from 3.78mln, with each of the preceding 3 months also revised up).

- The uptick in January meant the highest sales volume since August 2023, but to put this into context, it is just months after briefly hitting the lowest reading post-2010 (3.85mln in Oct 2023).

- From a regional perspective, sales increased in each of the Midwest, South, and West regions, but were flat in the Northeast.

- With supply remaining constrained as existing homeowners resist giving up long-term fixed mortgages at lower-than-prevailing rates, months of inventory fell by 0.1 month to 3.0, the lowest since April 2023.

- Median sales prices rose for a 7th consecutive month, by 5.1% to $379,100, but reflective of the inert mortgage borrowing market, 32% of transactions in January were all-cash, up from 29% a year ago.

- With mortgage rates beginning to tick higher again as implied Fed rate cut probabilities fade, pulling back on borrowing activity (as we pointed out in our note on MBA mortgage applications on Wednesday), it's unlikely that existing home sales will see a resurgence in the near future.

- Conversely, new home sales (data out Monday) - which are less affected by the above dynamics - are expected to maintain their general uptrend since mid-2022 (+3.0% seen in Jan, after +8.0% in Dec).

Source: NAR, MNI

Source: NAR, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok