Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

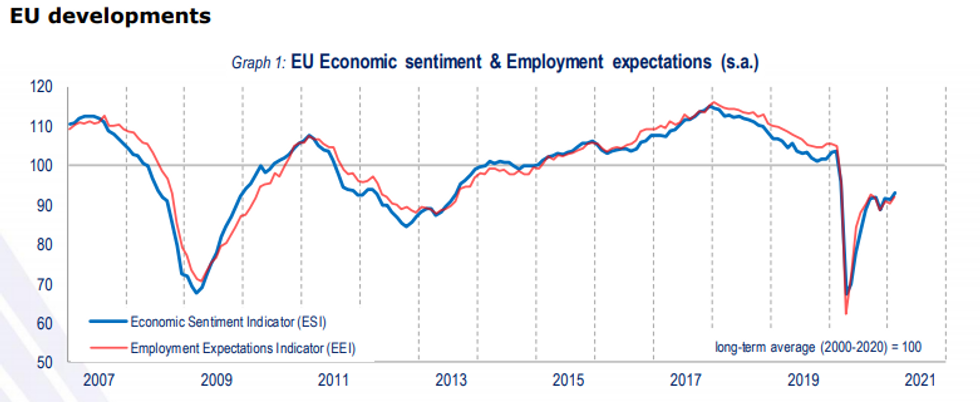

Economic Sentiment Indicator (ESI): 93.4; Prev (Jan): 91.5

Consumer: -14.8(Jan: -15.5); Industry: -3.3 (Jan: -6.1); Services: -17.1 (Jan: -17.7); Retail: -19.1 (Jan: -18.5); Construction: -7.5 (Jan: -7.7)

- The EZ ESI ticked up 1.9pt to 93.4 in Feb, showing the highest level since Mar 2020 and coming in stronger than markets expected (BBG: 92.0).

- Among the largest EZ economies, the ESI saw the largest gains in Poland (+4.7pt), Italy (+4.4pt) and Germany (+3.0pt), while it fell sharply in Spain (-3.2pt) and to a lesser extent in the Netherlands (-1.3pt).

- Industrial sentiment was the main driver of Feb's increase, rising to the highest level since Mar 2019 at -3.3.

- In line with the flash estimate, consumer confidence ticked up to -14.8, but remains well below the pre-pandemic level.

- While service confidence edged slightly higher by 0.6pt to -17.1, retail trade sentiment fell further to -19.1, its lowest level since Jun 2020.

- Both indicators remain far below the pre-crisis level as tight restrictions weigh on business activity in both sectors.

- The construction sector saw a small uptick in sentiment to -7.5, up from -7.7 seen in January.

- The employment expectations index increased to a four-month high of 90.9 in Feb, following Jan's decline to 89.1.

Source: European Commission

MNI London Bureau | +44 203-865-3814 | irene.prihoda@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok