Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

German factory orders for December easily beat expectations, rising by +2.7% Y/Y (vs -5.3% cons; -4.7% prior, revised from -4.4%) and +8.9% M/M (seasonally-adjusted; vs -0.2% cons; 0.0% prior, revised from +0.3%). For 2023 as a whole, factory orders declined -5.9% Y/Y.

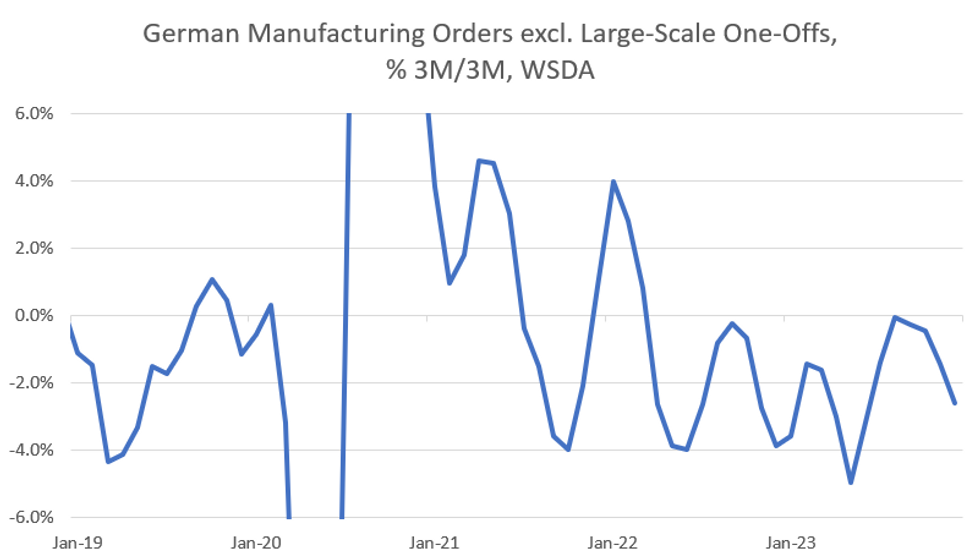

- However, the December beat was strongly driven by volatile large ticket items, particularly in the airplane sector. Excluding one-off big ticket items, "core" new orders declined -2.2% M/M (vs -0.8% prior), the 4th consecutive monthly drop, with the less volatile 3M/3M measure coming in at -2.6% (vs -1.4% prior), the lowest since June 2023. The level of core orders is at the lowest since the pandemic.

Looking at individual components, the "other vehicles" sector saw a jump of +110.9% M/M. This can be accounted for by large airlines including Turkish Airlines ordering more then 800 Airbus aircraft in the month (per Airbus data - total 2023 deliveries were at 735), which are partly manufactured in Germany.- Large one-off orders also drove the headline figure higher in the metal products and electrical equipment sectors. Consequently, investment goods and intermediate goods orders grew at +10.9% M/M and +8.3%, respectively. Consumption goods saw a decline of -1.3% M/M.

- Looking at a geographical split, domestic orders climbed by +9.4% M/M, up for the 2nd consecutive month. Foreign orders increased +8.5% M/M, driven by Eurozone orders increasing +34.5% (non-Eurozone at -7.5% M/M).

- Even though the headline suggests a clear uptick in activity compared to last month, the underlying "core" measures rather point towards ongoing weakness in German industrial activity.

- Indeed, real turnover in manufacturing fell -0.1% M/M, suggesting that the rather weak consensus estimate of Wednesday's industrial production data (-0.5% M/M expected, after -0.7% in Nov) might be well justified.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok