Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

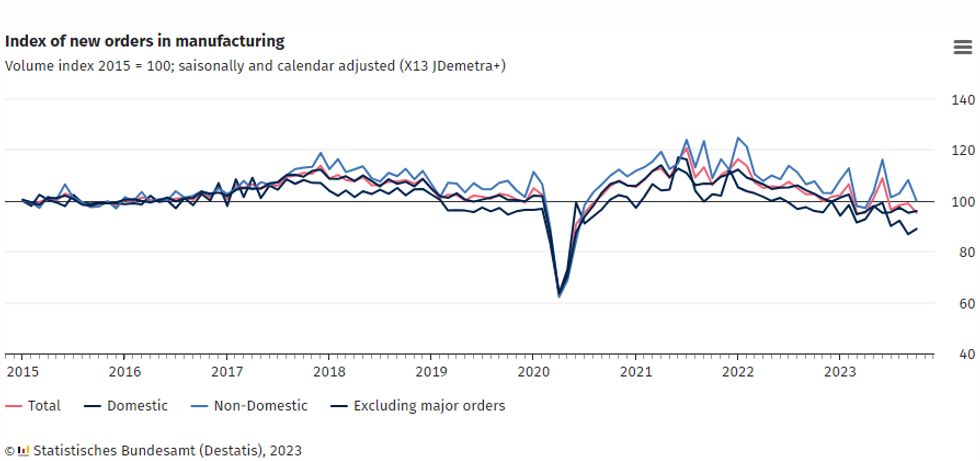

German factory orders clearly missed expectations in October, at -3.7% M/M seasonally/calendar adjusted (+0.2% consensus, +0.7% previous, upwardly revised from +0.2%) and -7.3% Y/Y on a calendar-adjusted basis (-3.9% consensus, -3.8% previous, revised from -4.3%).

- Total orders are now broadly on a level with their value in July 2020 (Index 95.3 vs 95.2).

- However, the drop was driven by a decline in one-off large-scale items, which are volatile. Excluding such big-ticket orders, "core" new orders rose +0.7% M/M, which was actually a significant improvement from -2.2% in September. The level of core new orders has been fairly steady since Q1 despite significant headline volatility. On a yearly basis, the core measure change ticked up by around two percentage points compared to September though remains negative (-6.6% Y/Y vs -8.5%).

- Foreign orders decreased by -7.6% M/M, contrasting with domestic orders which increased by +2.4%.

- Looking at individual sectors, manufacturing of machinery and equipment was particularly weak at -13.5% M/M. Other vehicle production (airplanes, ships, trains) was driven higher however by one-off orders, coming in at +20.2% M/M.

- Real turnover also started Q4 on a weak note at -0.5% M/M after a -1.4% decline in September (vs -1.6% in the provisional figure).

- Overall, the data are volatile but the core readings continue to suggest that in line with other recent data (eg November manufacturing PMI and the October trade balance), economic activity in Germany might be flattening out at a weak level.

- That said, Industrial Production for October is due tomorrow and today's figures suggest downside risks versus current consensus (-0.2% M/M, -1.4% Aug) given the soft manufacturing data in particular.

Destatis

Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok