Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

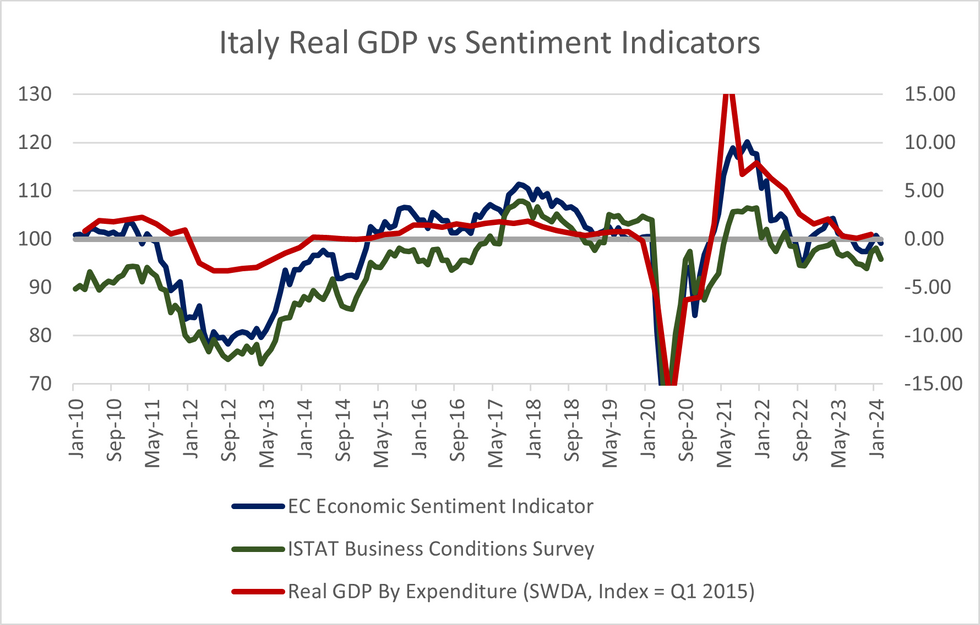

Italian business sentiment ticked lower in the ISTAT and EC surveys released this morning. Across both releases, all industry sub-components saw falls in overall sentiment, but retail services stood out with the largest moves lower. Overall, the surveys remain at levels consistent with muted growth prospects to start 2024.

- Analysts currently forecast Q1 '24 real GDP at 0.1% Q/Q (vs 0.2% in the Q4 '23 flash release).

- ISTAT business confidence fell to 95.8 (vs 97.9 in Jan), while the EC sentiment indicator fell to 99.2 (vs 100.8 in Jan). This reverses much of the uptick seen in December (for ISTAT) and January (for EC).

- Expected prices amongst services respondents moved up a touch in both surveys. The ISTAT reading of 10.4 (vs 9.8 in Jan) is a touch below the 2023 average of 10.7 while the EC's 12.1 (vs 11.2 prior) remains above the 2023 average of 10.6.

- A reminder that the January services PMI signalled rising prices amongst services producers as a result of "increasing fuel prices, utility costs and salaries".

- Expected prices amongst retailers fell in both surveys.

- The EC's expected employment indicator fell to 106.4 in February (vs 107.5 prior), remaining below the 2023 average of 108.1. Expected employment rose amongst retailers but fell for services providers in both surveys.

- The EC's labour hoarding indicator reversed January's fall to rise back to 8.4 (vs 7.7 in Jan, 8.4 in Dec), rising in all industries other than services.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok