Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

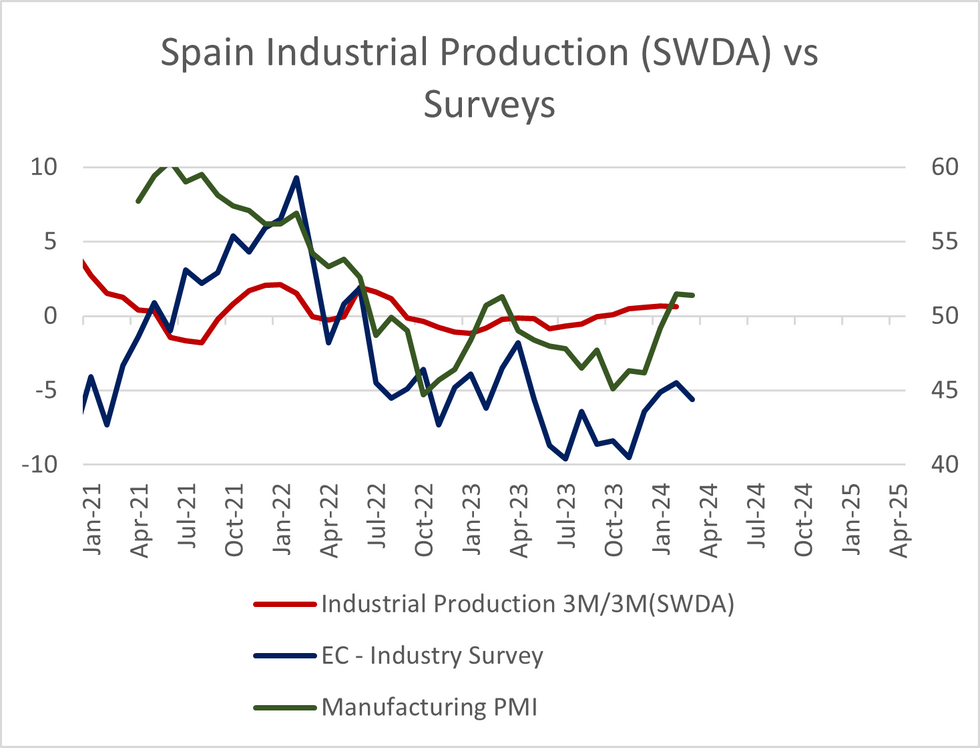

Spanish February industrial production surprised to the upside, printing at 1.5% SWDA Y/Y (vs -0.4% cons). Last month’s release was also revised higher, to 0.3% Y/Y (vs -0.6% initially).

- The print confirms the outperformance that has been signalled in recent Spanish survey data, with the manufacturing PMI and the EC industry survey both rising in February.

- Looking ahead, the manufacturing PMI remained in expansionary territory in March (51.4 vs 51.5 in February). While the EC’s industry survey was contractionary at -5.6 (vs -4.5 in Feb), it remained above the 2023 average of -6.6.

- On a 3m/3m SWDA basis, IP has been positive for the last 5 months, printing at 0.6% in February (vs 0.7% prior).

- Looking at the sub-components, consumer goods drove this month’s strength in the annual print, rising 3.3% Y/Y (vs -0.6% prior).

- On an SWDA monthly basis, production rose 0.7% M/M (vs 0.2% cons, a 0.2pp upwardly revised 0.6% prior).

- Spain only makes up around 8% of Eurozone industrial production (February data due April 15), with Germany’s data (April 8) carrying a much more significant 39% weighting.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok