Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

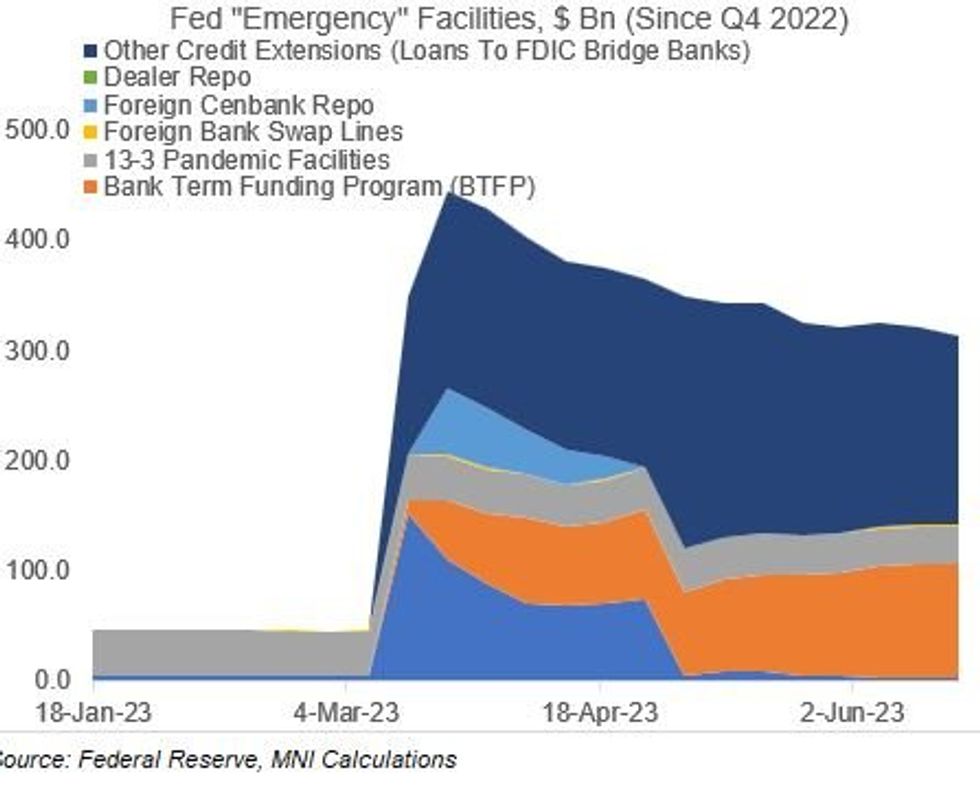

Fed lending / liquidity extension to banks continues to fade as banking sector stress appears to be abating, with a continued shift away from Discount Window usage and toward takeup of the Bank Term Funding Program (BTFP).

- Total takeup of extraordinary and lending facilities at the Fed has fallen to $313B from the March peak of $445B.In combination with the fall in Fed assets via quantitative tightening, which includes $15B over the past week and $68B in the past month, the drop in lending takeup means total Fed assets have fallen to $8.36T vs the $8.73T peak in mid-March.

- That’s not far from the $8.34T seen just before the SVB / bank crisis in March, and we should continue to see new cycle lows so long as liquidity provision growth remains subdued.

- Total usage of liquidity/financial stability facilities fell $8.3B in the week to Jun 21, bringing the 4-week fall to $11.4B.

- Discount window usage is $3.2B, down $0.4B on the week and $1.0B on the month - and almost nonexistent versus the $153B peak. Conversely the BTFP continues to hit new highs, up $0.8B on the week to $102.7B - a gain of $10.78B in the past month.

- The overall decline in lending was due to $8.1B lower usage of "other credit extensions" (the line item for Fed lending to FDIC bridge bank entities for resolution purposes), off $20.3B on the month and vs a $228.2B May peak reached after the First Republic closure).

- More tables/charts are available in our Fed Balance Sheet Tracker.

Source: Federal Reserve, MNI

Source: Federal Reserve, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok