Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE DATA

France Final HICP data for March confirmed the flash reading on an annual basis at 2.4% Y/Y (3.2% Feb), though the non-seasonally adjusted M/M figure came in slightly softer than flash at 0.2% (0.3% flash, 0.9% Feb). Recall that the flash French Y/Y print was 0.4pp below-expected, and the first below 3% since September 2021, helping set the tone for a lower-than-consensus Eurozone-wide print the following week.

- This was a broadly disinflationary report: as was suspected upon the flash release, the slowdown in inflation was driven by both non-core and core components (a breakdown was not available in the flash).

- Core inflation slowed to 2.2% Y/Y (vs 2.6% prior), with a slight softening in services inflation to 3% Y/Y (vs 3.2% prior), with an unchanged non-seasonally adjusted monthly reading (0.1% M/M). Manufactured goods prices pulled back again, to 0.1% Y/Y (0.4% prior), with the smallest M/M increase since 2014 (1.5%, not seasonally adjusted).

- Similarly, food prices disinflated on an annual basis to 1.7% Y/Y (vs 3.6% prior) - the twelfth consecutive deceleration. in addition, energy prices continue to slow, with an increase in energy prices of 3.4% in March (vs 4.3% prior). Year-earlier base effects played a key role.

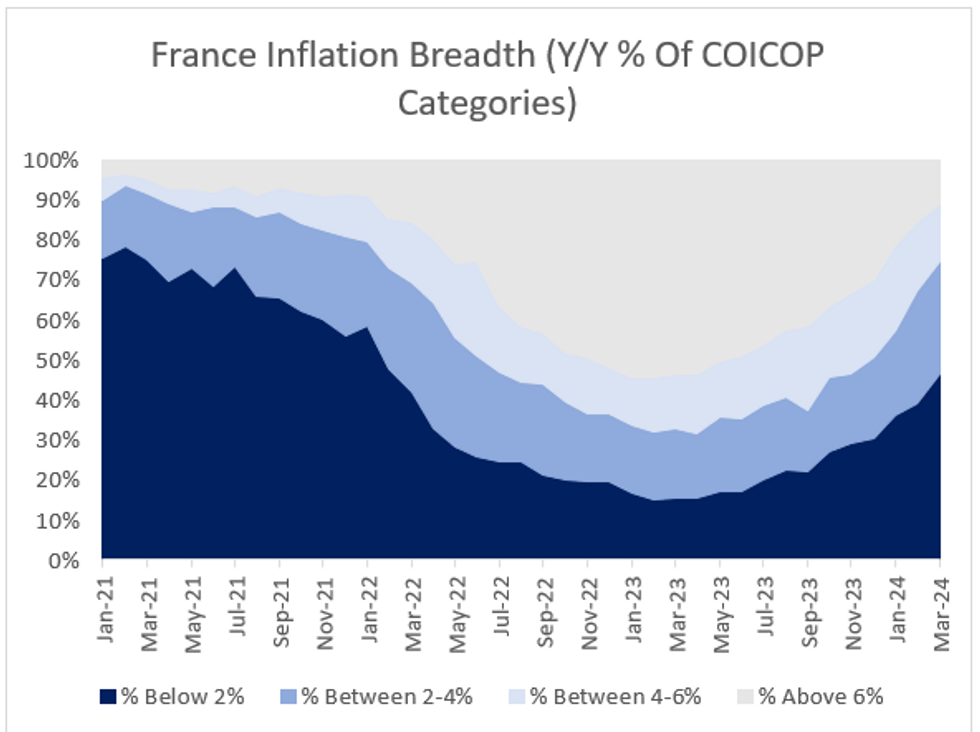

- Looking at the breadth of inflation, MNI's analysis shows that the proportion of components with inflation below 2% rose from 39% in February to 46% March - the highest since Feb 2022. Meanwhile, the proportion of components with inflation above 6% declined to 11% from 15% in February - the lowest level since January 2022.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok