Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

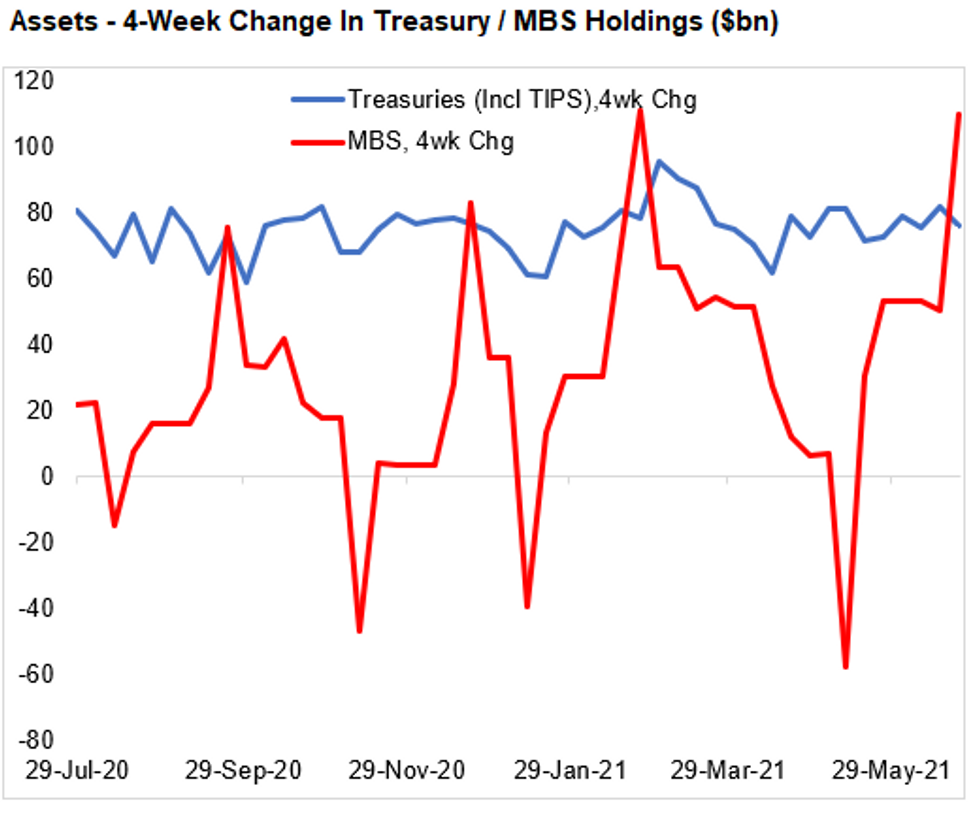

The FOMC revealed it had started "talking about talking" about tapering asset purchases at the June 15-16 meeting, putting into play several questions on the topic of asset purchase reduction.

- Tapering will be well underway and probably over by the time the FOMC lifts off on rate hikes, so the Fed's dot plot which includes 2 2023 hikes means that as it stands, a taper timeline is set to be roughly in line with pre-June FOMC expectations (late-2021 announcement for late 2021/early 2022 start) barring downside surprises in the data.

- The balance sheet looks set to continue expanding monthly by $120-130bln (the rate of growth seen over the past 3 months) through the rest of 2021, but beyond that, the trajectory is in question.

Source: Federal Reserve, MNI

Source: Federal Reserve, MNI

- It's no guarantee that the Fed will wait for the taper to end before hiking: our policy team reports some former Fed officials anticipate economic conditions will warrant interest rate increases as early as 2022 following a tapering decision to be delivered toward the end of this year, leaving little or no time separating the two processes.

- Another question is the composition of any taper – several FOMC members have had to fend off questions on MBS purchases, which as we highlighted in our last Balance Sheet update could be tapered prior / more quickly than the Treasury portion of the asset purchase program.

| Assets | Total | Nominal Tsys | TIPS | Bills | MBS+Agencies | 13-3 Facilities | Liquidity Facilities | Other* |

| Last Week's Net Change (USDbn) | 37.7 | 6.6 | 2.0 | - | 26.0 | 0.5 | - 1.3 | |

| 4-Week Net Change (USD bn) | 198.4 | 66.2 | 6.4 | - | 109.9 | 2.5 | 2.4 | |

| Total Holdings (USD bn) | 8,101.9 | 4,434.0 | 349.3 | 326.0 | 2,356.5 | 143.6 | 87.1 | 405.4 |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok