Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CREDIT MACRO

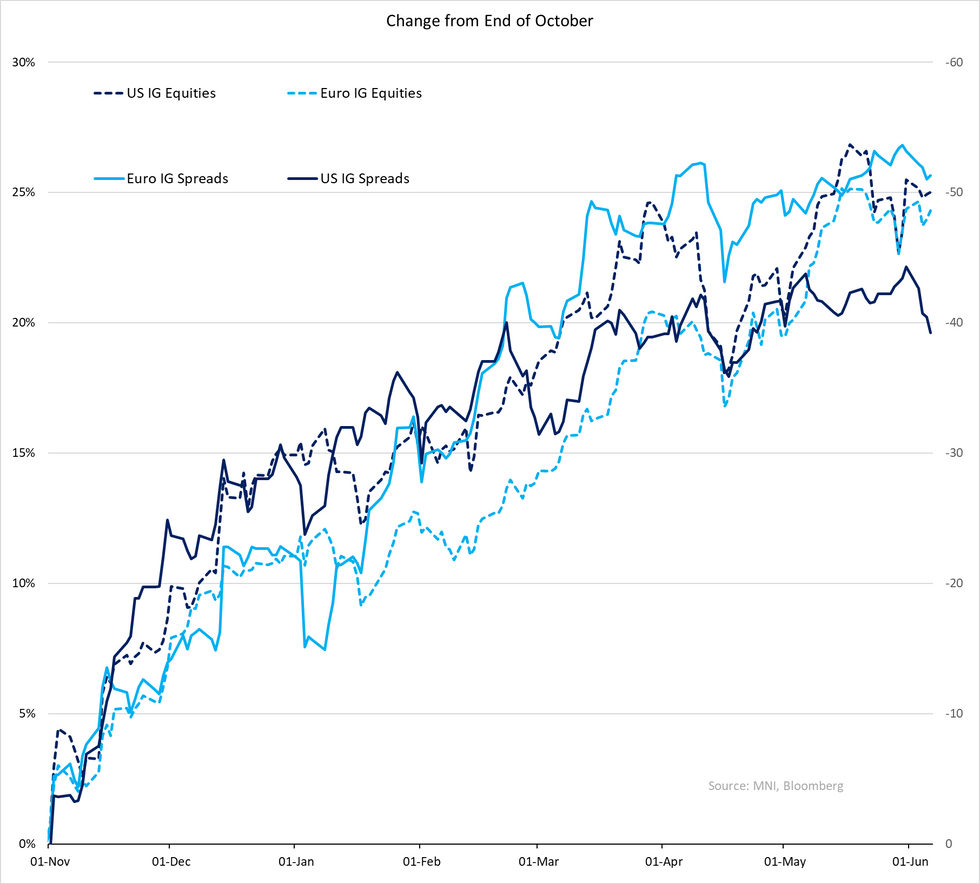

- Inflows in $IG/HY, small outflows from €IG/HY & £IG - those are reported to the week ending Wednesday. NFP linked rates moves (bunds +8, USTs +13) will have the final say. YTD total returns were already flirting around breakeven levels, todays moves if held onto will drag those negative again.

- To Wednesday govvie inflows continued, Euro in particular seeing a spike perhaps in anticipation of ECB. It was the first of the Big 3 to cut rates and gave a clear example that early cuts does not imply better total returns ahead for credit; expectations out of it were a hawkish dragging bunds +4 higher and €IG total returns -18bps.

- Supply has come firmer than expected; € & £ IG/HY incl. covered at €30b (vs. c~€23b) while $IG was at $33b (c$20b). NICs have continued to avg. higher across both regions, book cover hanging at the lower end locally, $IG tad firmer around 3x.

- Expectations for next week stay unch at ~€20b with slight skew to financials. $IG also unch at $20b.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok