Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China Q1 GDP was stronger than expected, up 1.6% q/q (forecast +1.5%), while Q4 from last year was also revised higher to 1.2% (from 1.0% originally reported). Y/Y growth came in at 5.3% versus 4.8% forecast. This keeps y/y momentum around the pace from H2 2023. Still the monthly March activity figures suggest some lost of momentum as we progressed through Q1.

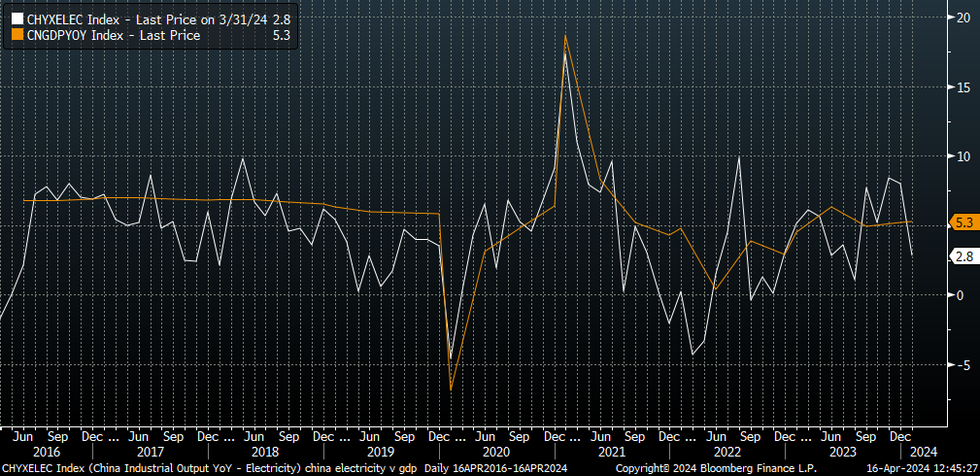

- IP rose 4.5% y/y, versus 6.0% forecast. Weakness was evident in the commodity space, while cement fell -22% y/y. Mobile phones fell as did cars (-0.2% y/y) but NEV's were still positive +33.5% y/y, but down from the pace at the end of last year. Electricity production eased back to 2.8% y/y, also off late 2023 highs of +8%.

- The chart below overlays this production metric against y/y GDP growth.

- In terms of retail sales, we eased back to 3.1%, against a 4.8% forecast. Consumer spending remains somewhat of a weak spot in the economy. We had slower spending related to restaurants and automobiles.

- Fixed asset investment was better than expected at 4.5% ytd y/y (4.0% forecast). State owned enterprises continue to drive the recovery, up to 7.8%, while private enterprises saw a more modest 0.5% ytd y/y. Investment was firm across most sub categories.

- Property investment was weaker at -9.5% ytd y/y, versus -9.0% in Feb. The detail showed continued deep y/y falls across the sub-categories. New home sales fell -30.7% ytd y/y.

- The jobless rate edged down to 5.2%, in line with forecast (prior was 5.3%).

Fig 1: China Electricity Production & GDP Growth Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok