Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

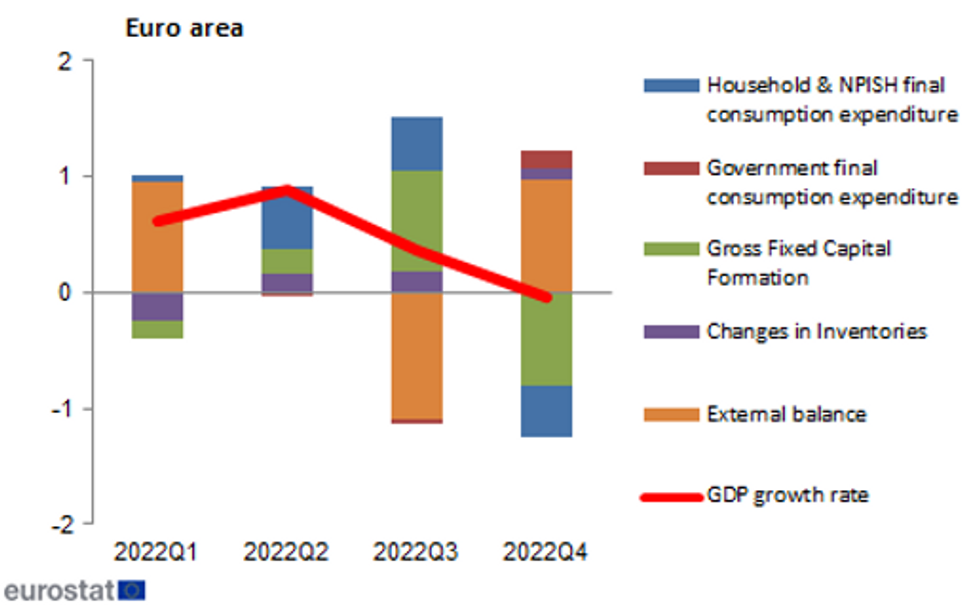

EUROZONE Q4 GDP 0.0% (=FCST, VS +0.1% FLASH); Q3 +0.4% Q/Q

EUROZONE Q4 GDP +1.8% (FLASH +1.9%); Q3 +2.4% Y/Y

- The euro area stalled in the Q4 final GDP print, after GDP was downgraded by 0.1pp on both the Q/Q and Y/Y headline figures. This was largely in line with expectations following the 0.2pp downwards revision to German GDP.

- The component breakdown confirmed that private spending was particularly weak into year-end, as persistent inflationary pressures and weak consumer sentiment continue to reduce spending appetite.

- Q4 household final consumption expenditure fell -0.9% q/q, after +0.9% q/q in Q3, accounting for -0.4pp on the headline q/q GDP figure.

- Gross fixed capital formation represented the largest drag to Q4 GDP (-0.8pp). Gross fixed capital formation contracted by -3.6% q/q, but was largely just a reversal of the Q3 boost.

- Government spending rose +0.7% q/q, adding +0.2pp to headline GDP, whilst the external balance contributed +1.0pp to Q4 GDP.

- As such, this data implies the eurozone Q4 q/q print was largely propped up by lower imports and stronger government spending in Q4.

Contributions to growth over previous quarter:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok