Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Global Morning Briefing

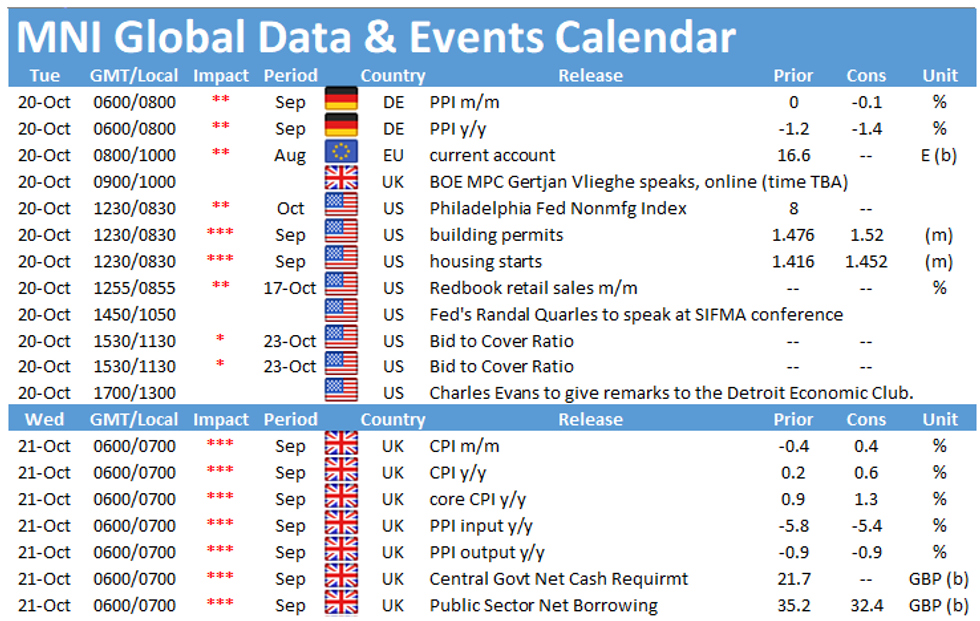

Tuesday sees a quiet schedule in terms of data releases. The main event to look out for in Europe is the release of the German producer price inflation at 0700BST. In the US the publication of housing starts and building permits as well as the Philadelphia Fed non-manufacturing survey will be closely followed at 1330BST.

German PPI seen falling again

German producer prices declined by 1.2% year-on-year in August, marking the seventh consecutive decrease. Energy inflation continued to be the main reason for the decline with energy prices being 3.9% lower compared to a year ago. In September markets expect another fall in the annual PPI by 1.4%. Monthly producer prices came in flat in August, following a small uptick in July. However, markets look for a slight downtick by 0.1% in September. Survey evidence is in line with market forecasts. Germany's manufacturing PMI noted another decline in prices paid for inputs in September with firms mentioning that the stronger euro reduced the cost of imported goods and that market prices for some commodities were lower.

US housing starts seen rising in September

Privately-owned housing starts are forecast to increase to an annual rate of 1,455,000 in September, up from 1,416,000 in August, which would be a 2.5% uptick. Meanwhile, building permits are projected to edge up 3.0% in September after falling by 0.9% on a monthly basis in August. Building permits recorded an annual rate of 1,470,000 and markets expect the figure to rise to 1,520,000 in September. While building permits registered 0.1% below the level seen in August 2019, housing starts were 2.8% higher than a year ago.

Philadelphia Fed non-manufacturing index rose in September

The Philadelphia Fed non-manufacturing business outlook survey showed further improvements in the sector with a sharp uptick of the general business activity index for the region to 8.0 in September, up from 1.6 in August. At the firm level, the current general activity index increased to 20.4 in September after recording 17.9 in August. Firms expect business conditions over the next six months to improve further, as the future activity index rose. According to the preliminary Michigan sentiment index, consumer sentiment ticked up slightly which bodes well with activity in the nonmanufacturing sector. Meanwhile, the New York business leaders survey was muted in October, as business climate little changed compared to the previous month.

Tuesday's events calendar throws up some speeches of note, including speakers such as BOE's Gertjan Vlieghe, Chicago Fed's Charles Evans, New York Fed's Daleep Singh, Atlanta Fed's Raphael Bostic and Fed's Randal Quarles and Lael Brainard.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.