Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

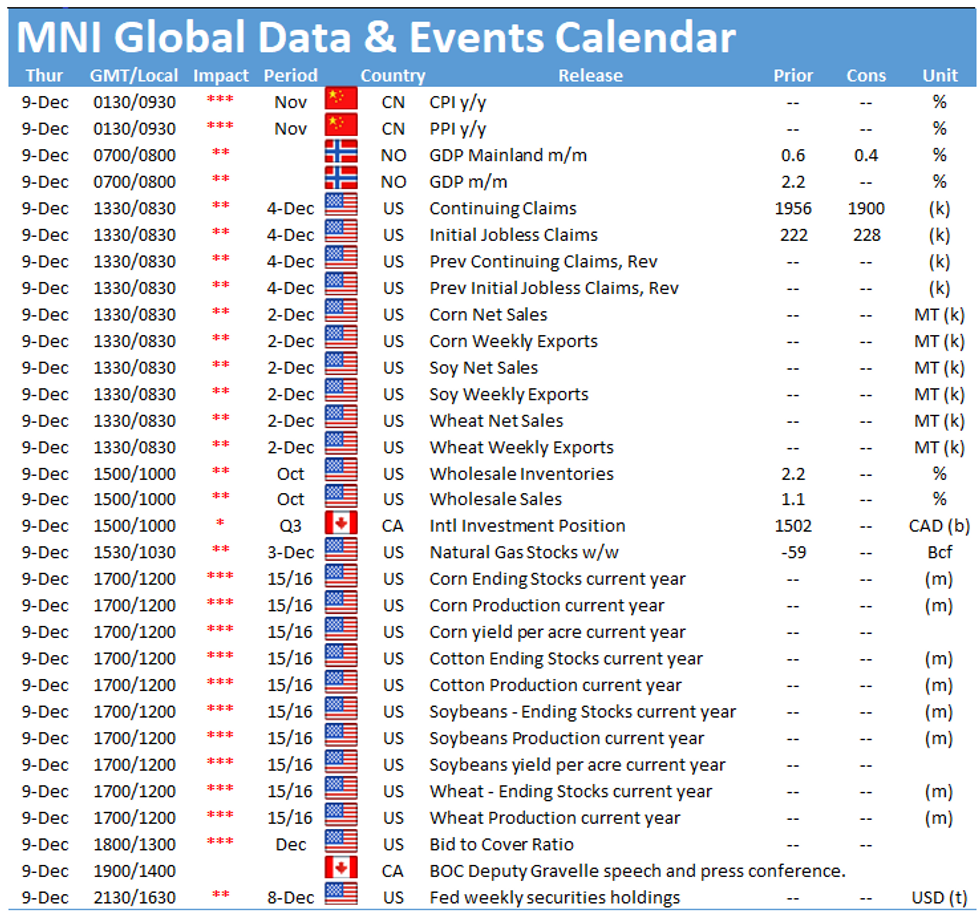

Thursday’s data is relatively light, with key focus on Germany and the US.

Norway GDP (0700 GMT)

Norway’s mainland GDP is forecasted to slow to 0.4% m/m in October, maintaining a slight downward trend from 0.6% in September and 1.0% in August. However, the 2.6% Q3 expansion implies the economy remains strong due to high employment rates and strong service sector expansion.

Germany trade data looks a little more optimistic (0700 GMT)

Market’s will be focus early attention on German trade data Analysts predict exports to rise to 0.8% for October’s monthly reading, up from -0.7% m/m in September. This comes following slight easing of supply bottlenecks whereby the automotive and machinery industries made significant recoveries. Imports are predicted to rise too (albeit less substantially) to 0.4% m/m in October, compared to 0.1% m/m in September.

Germany’s trade balance is forecast to narrow further in October, dropping to E14.3bln surplus from E16.2bln in September. The current accounts balance is similarly projected to have fallen, with the October reading predicted to be E17.0bln for October, down from E19.6bln in September.

US labour market improving marginally (1330 GMT)

US employment continues to rebound amid nationwide labour shortages, incited by demographic shifts and higher demand for goods. Initial jobless claims for last week are set to reduce marginally to 220,000 down from 222,000 the week prior, which came following a five-year low of 194,000 in the week before. Similarly, continuing claims look likely to reduce to around 1,910,000 for the final week of November compared to the prior reading of 1,956,000.

US wholesale inventories increase (1500 GMT)

Wholesale trade sales and inventories are forecasted to come in at 1.0% and 2.2% m/m respectively for October, compared to 1.1% in and 1.4 % in September. The jump in inventories was highlighted by the Chicago Business Barometer resulting from stockpiling to buffer for supply chain disruptions.

Today we see only one policymaker speech from Bank of Canada’s Deputy Gravelle.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.