Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US OUTLOOK/OPINION

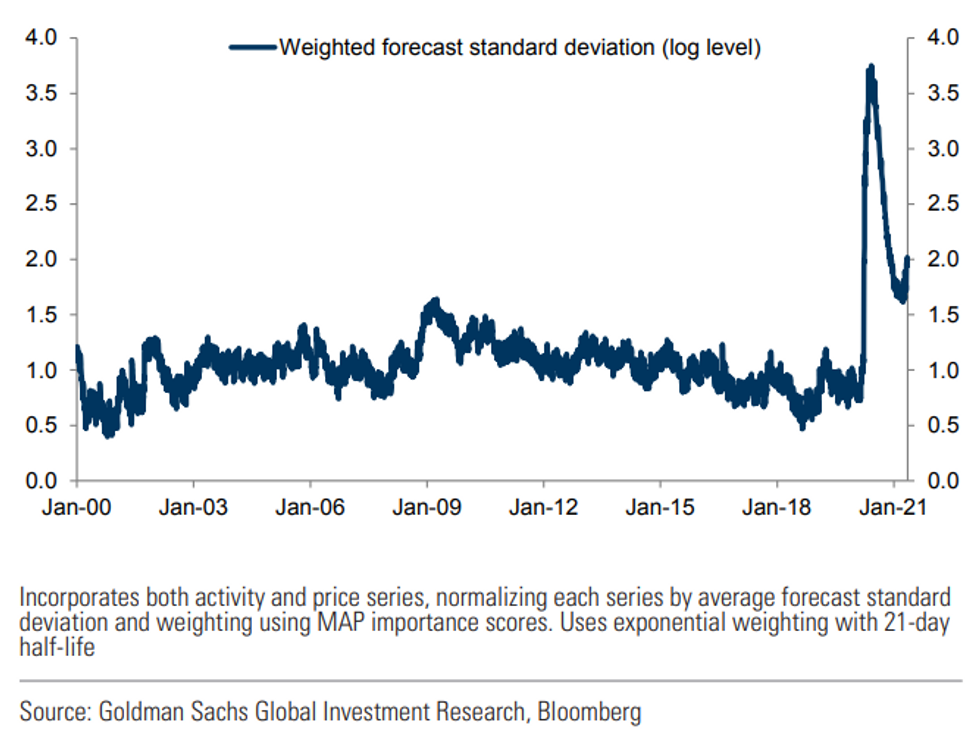

In a note out early Thursday, Goldman Sachs assessed how US Tsy yields are likely to respond to data surprises as we begin to get 2Q 2021 data (noting that yields have moved lower despite upside data surprises for mostly 1Q data in April).

- With such wide dispersions around estimates as we come out of a once-in-a-lifetime pandemic, Goldman looks at the historical data and concludes that surprises amid great uncertainty matter somewhat less to market movements: "yield sensitivity to data surprises tends to decline at higher levels of forecast uncertainty, suggesting that until there is some convergence in projections, yield responses to data releases may remain muted by historical standards".

- In other words, "what may be a market-moving surprise in the context of low levels of dispersion among forecasters is little more than noise when said dispersion is high".

- It may take until later in the year before "convergence among forecasters" occurs.

- That gets us to Friday's nonfarm payrolls reading: they note that standard deviations for the upcoming April release are more than 3 times their historical average, so a surprise number may not have as big an impact as it would in more "normal" times.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok