Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

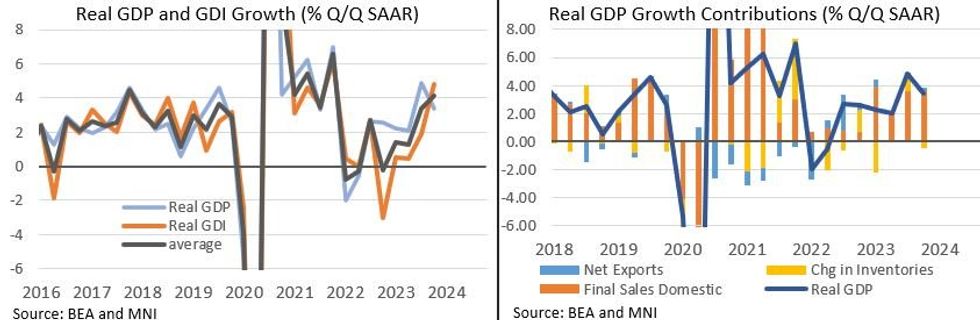

Real GDP was revised up by 0.2pp in the final reading for 4Q23, with quarterly annualized growth of 3.4%. The internals of the revision were broad-based, including a very strong gross domestic income reading.

- Private consumption and fixed investment each contributed an additional 0.2pp versus the previous estimate more than offsetting a bigger drag from inventories, and less of a contribution from net exports.

- The headline PCE price index was unrevised at 1.6%, but more attention was placed on the core PCE inflation reading which was revised down a tick to 2.0% from 2.1%.

- The figures still represent a slowdown from the 4.9% Q/Q SAAR print in 3Q, but the deceleration was a little less pronounced than previously estimated (and the final print was above the expectation of an unrevised 3.2% reading).

- Of particular note in this release was that gross domestic income - which in theory should be equal to GDP - rose by 4.8%, up from 1.9% in the prior quarter and the strongest reading since 4Q21, with domestic corporate profits up sharply.

- This brought the average of GDP and GDI in the quarter to 4.1%, the highest since 4Q21 - and helping to bridge the discrepancy between outperforming GDP and underperforming GDI. This was the first quarter since 2Q 2022 that GDI came in above GDP.

- This gap had been identified by some as potentially pointing to a weaker economy than suggested by the GDP measure - but this has so far not materialized. And note that the prior quarter had already seen an upward revision to GDI in last month's national accounts release (0.4pp to 1.9%).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok