Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EMERGING MARKETS

MNI (London)

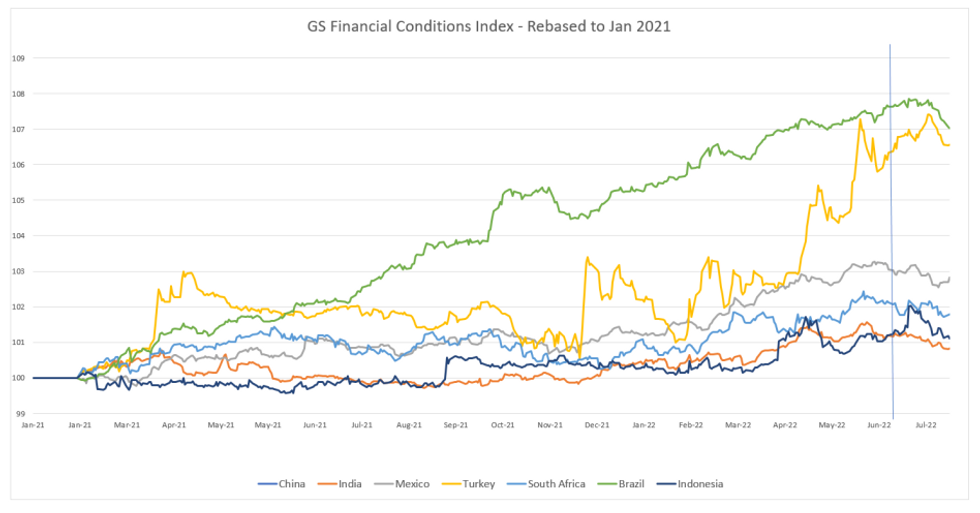

- Brazil has seen the largest financial conditions tightening since the beginning of 2021 according to the GS FCI, with a 7.9% increase from January 2021 to the mid-July high. The speed of tightening by the Brazilian central bank is largely accountable for this sharp shift in tightness, hiking by 11.75% over this period.

- Following Brazil, GS FCI tightening over the period from Jan 2021 to June/July 2022 highs is Turkey (up 7.4% albeit largely due to economic instability powered by a stark depreciation of the lira), Mexico (+3.3%) and South Africa (+2.4%).

- The GS FCI has seen a recent shift towards a loosening trajectory since mid-July. With both Brazil and Indonesia seeing some of the swiftest loosening, commodity exporters could have the upper hand here, however it is too early to confirm the onset of a more persistent downwards trajectory.

- Financial conditions seeing some relief again is underpinned by the USD coming off its peak and equities coming off bottoms following the substantial sell-off. Furthermore, markets have already largely priced in the bulk of US hiking. This morning the PBOC unexpectedly cut rates after a slew of weak economic data, adding to the general consensus of global monetary tightening coming to a close around year-end as real rates begin to move out of negative territory (more on this here).

- Despite this year's rash global tightening, financial conditions remain relatively loose for EMs compared to historical levels.

Source: MNI / Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok