Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

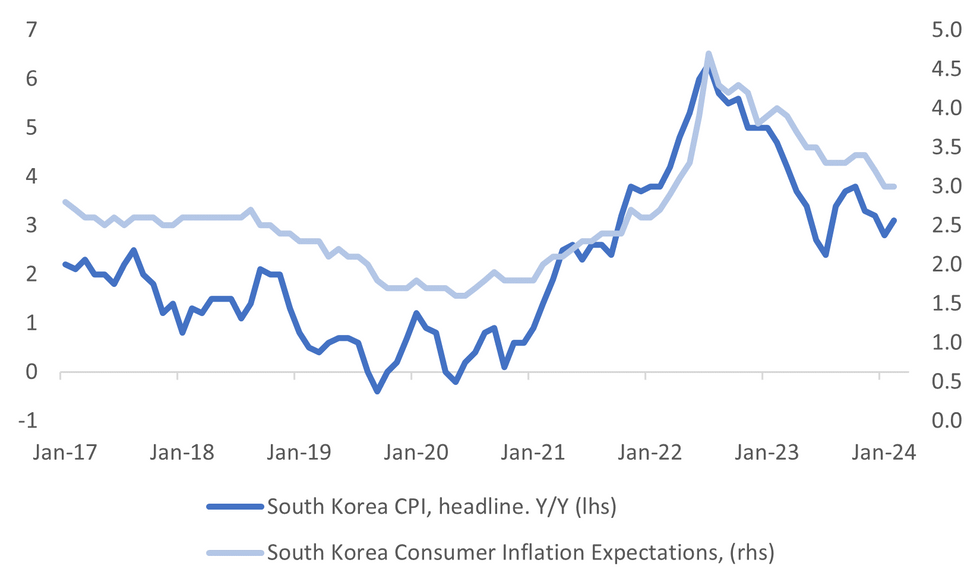

South Korean Feb CPI was a touch above expectations in terms of headline pressures. We rose 3.1% in y/y terms, versus 3.0% forecast and 2.8% prior. The m/m outcome was in line at 0.5%, while core (ex food and energy) also met expectations at 2.5%y/y (which was also the Jan reading).

- The chart below plots y/y headline CPI against consumer inflation expectations. We are well off 2022 highs, but not yet back to the 2% BoK inflation target, particularly for expectations.

- In terms of the detail, the biggest m/m gains in Feb were for food, +1.4% and transport, +1.5%. Recreation also rose 1.0% m/m. These moves may have been driven by the LNY.

- Only two categories saw falls in m/m terms, while other categories saw only modest rises or flat outcomes in the month.

- In y/y terms, food +6.9% and clothing at 5.7%, are recording the strongest gains.

- For the BOK, they are likely to remain in watch and wait mode, to see if pressures, particularly those potentially related to LNY tick down in March.

Fig 1: South Korea CPI Y/Y & Consumer Inflation Expectations

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok