Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HEALTHCARE

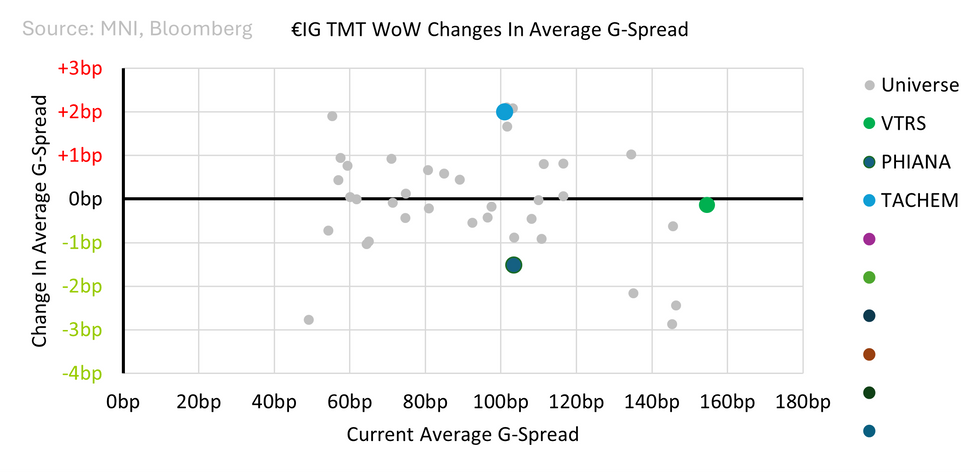

Healthcare Sector: Week in Review

- Viatris VTRS suffered a -5% fall in the equity market this week as guidance was subdued following results. It is worth noting that the CEO reiterated its commitment to reduce debt which should at least be welcome news to the credit market. Given that S&P’s BBB- rating has a negative outlook this matters. Spreads were unchanged on the week.

- Eli Lilly LLY and Novo Nordisk NOVOB continued to power ahead with rises of c5% each but note that last Friday Amgen AMGN also rose 5% as it announced developments in the anti-obesity market. LLY and NOVOB will not be without competition forever.

- Takeda TACHEM bonds were +2 wider on the week as results came in as expected. Takeda (Baa1/BBB+) does trade wide to the single-A pharma issuers but there is little room for it to tighten from here in the near-term.

- Fresenius SE FREGR raised outlook for the full-year and were upbeat about the progress of its restructuring efforts. FREGR’s strategic exit from Vamed has been initiated and it will focus entirely on Kabi and Helios now.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok